Changed their mind!

At first, the insurance company promised to take responsibility for the accident and even approved car repairs that took nearly a month. But later, they suddenly called the client and claimed they would not cover the damages after all, arguing that the driver’s blood alcohol level must have been higher before the breathalyzer test.

The client’s actual test result was only 14 milligrams percent (mg%), well below the legal limit of 50 mg%, yet the company insisted that the level “must have exceeded 50 mg% before testing.” Using this reasoning, they refused to pay and told the client, “If you want to fight this, go find a lawyer and sue us.”

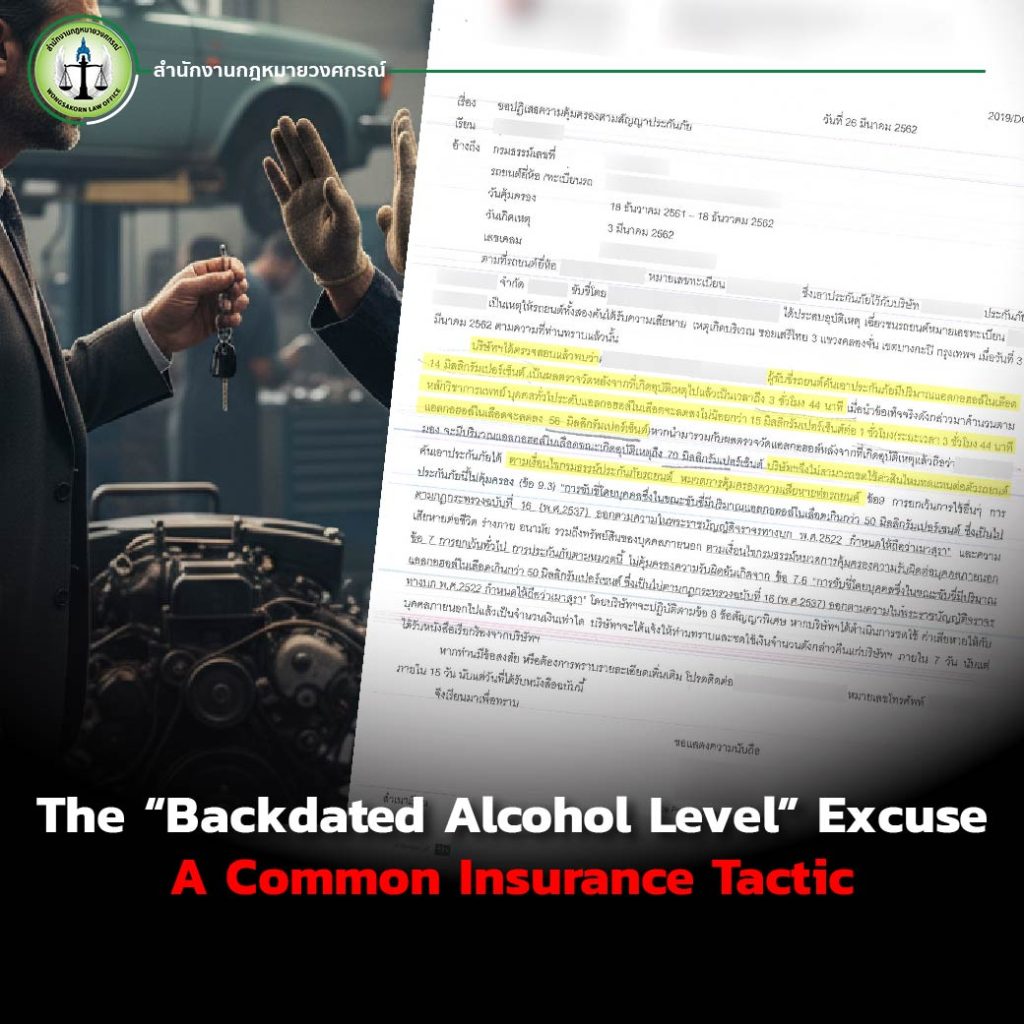

The “Backdated Alcohol Level” Excuse A Common Insurance Tactic

This isn’t an isolated case. Many accident victims have faced the same issue: insurers “recalculating” alcohol levels after the fact to justify denying payment. It’s become one of the most common and questionable tactics in the industry.

But for this particular client, it was shocking. He had trusted a seemingly reputable insurance company, believing they would stand by him. Instead, he was abandoned and accused unfairly of being intoxicated beyond the legal limit.

The Accident: A Minor Collision at 3 A.M.

The incident occurred around 3:00 a.m. The driver was heading home after a night out. Only about 100 meters from the venue, on a one-way street, his car brushed against a parked pickup truck that was sticking out into the lane. The collision caused only surface scratches along the side of the client’s vehicle, no dents, no severe damage.

The insurance company initially accepted responsibility and arranged for repairs, which took about a month. Then, out of the blue, they called back:

“We’re no longer responsible for repairing your car.”

The reason? A so-called retrospective alcohol analysis. Even though the actual breath test at the scene showed 14 mg%, the insurer claimed that “the driver’s alcohol level must have been over 50 mg% before testing.”

The client was stunned how they could retroactively raise the alcohol level just to deny coverage?

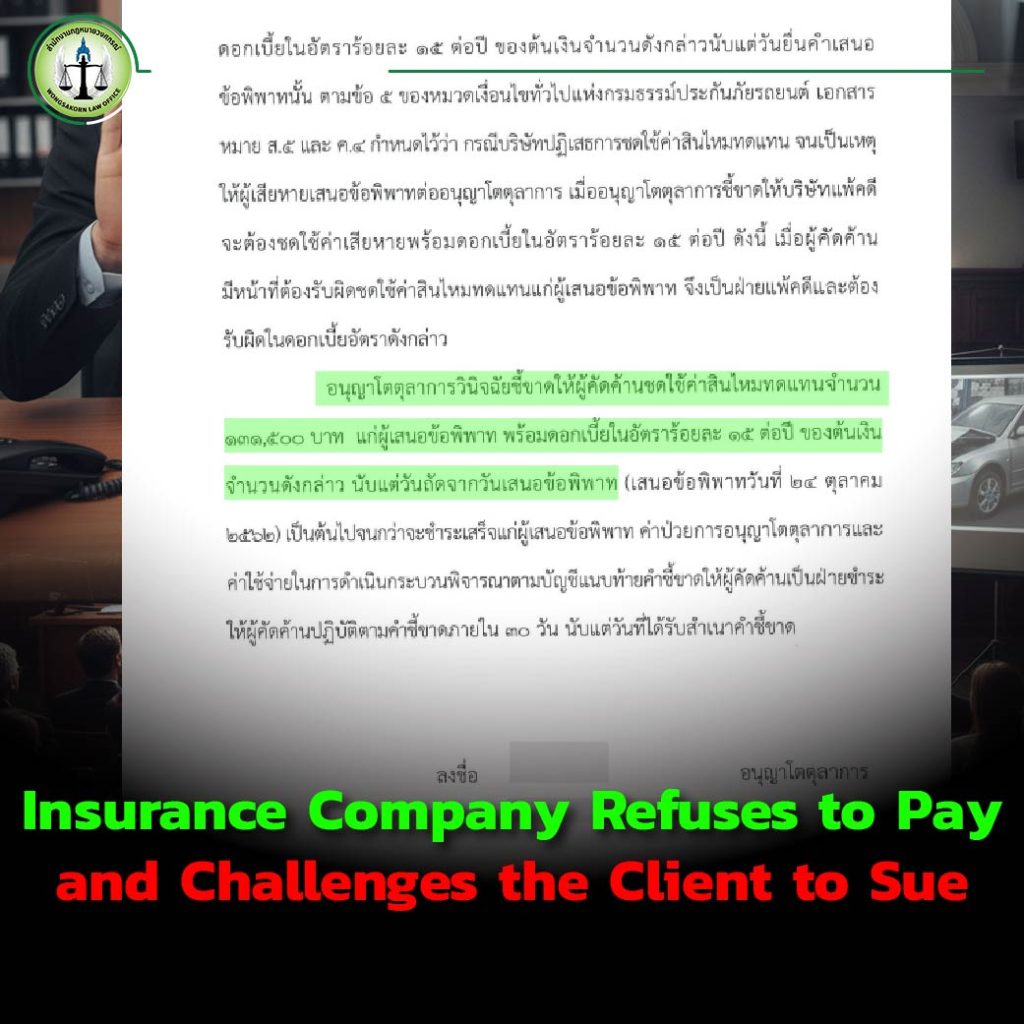

Insurance Company Refuses to Pay and Challenges the Client to Sue

As if denying coverage weren’t enough, the insurer told the client directly:

“Go hire a lawyer and sue us.”

They flatly refused to take responsibility, despite the police report clearly stating that the accident resulted from careless driving, not intoxication. The victim was left completely helpless and betrayed by the company that was supposed to protect him.

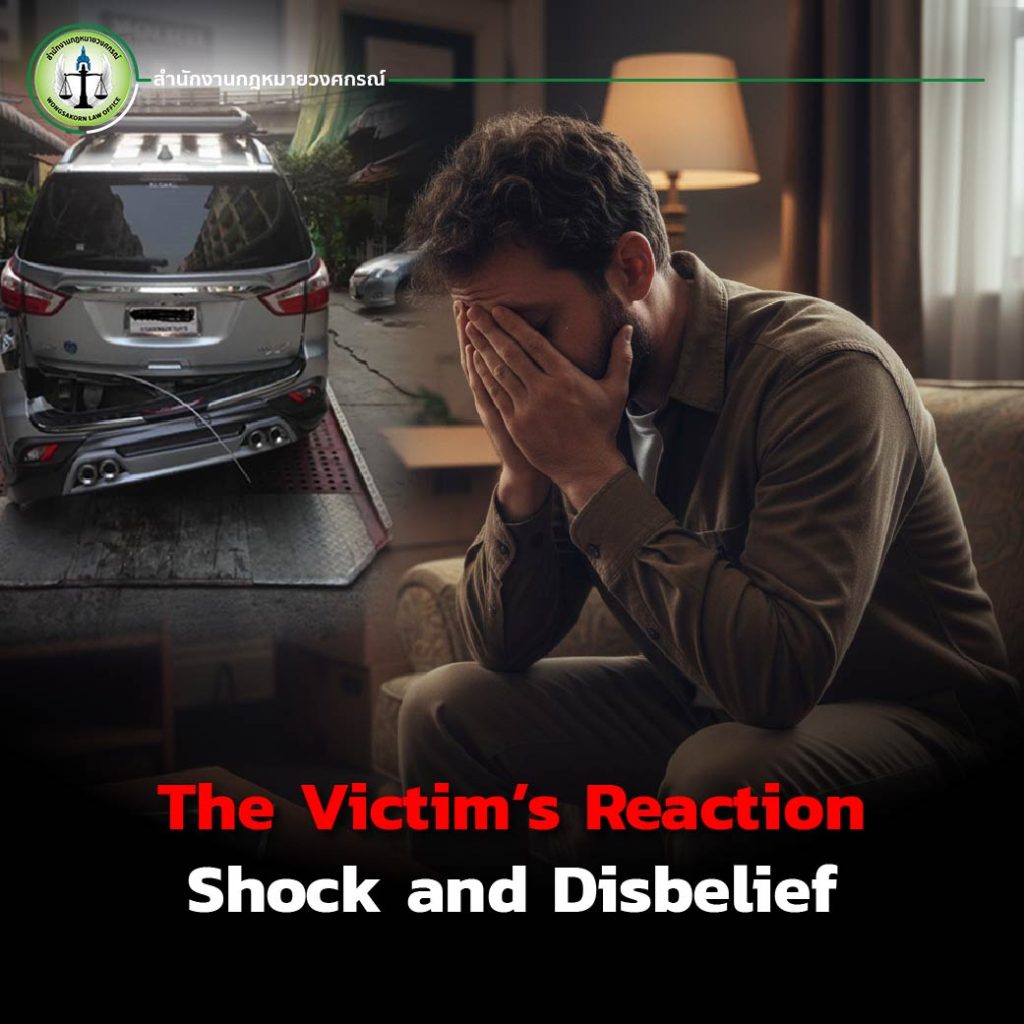

The Victim’s Reaction Shock and Disbelief

“I just don’t understand,” he said. “I paid for insurance so that the company would take care of me. My breath test was only 14 mg%, which is legal. Why are they refusing to help and leaving me to deal with everything alone?”

He had trusted the insurer, believing that his policy guaranteed protection. But instead, the company abandoned him mid-process even after his car had been in the repair shop for a month.

After the Denial Turning to a Lawyer for Help

After being told to “go sue,” the victim didn’t hesitate. He contacted the Lawyer Arm at Wongsakorn Law Office to handle the case. Having endured both the accident and the insurer’s betrayal, he realized that having a lawyer from the start would have saved him stress, time, and unnecessary financial loss.

Why Having a Lawyer from the Beginning Matters?

Don’t wait until the insurer pulls a trick like “backdating alcohol levels” before you seek legal help. Consulting a lawyer right after an accident gives you peace of mind and ensures your rights are protected.

Here’s why:

- You won’t have to negotiate directly with the insurance company or risk falling for their tactics.

- You save time when your lawyer will handle all communication, documentation, and follow-ups.

- A lawyer safeguards your rights and interests from day one until the case is fully resolved.

In short: a lawyer protects you before problems start, not just after they arise.

Legal Insight: Drunk Driving and Insurance Liability

Insurance companies often refuse to pay if the driver’s blood alcohol level exceeds 50 mg%, as this violates both insurance terms and traffic laws. Even with first-class coverage, insurers can deny payment to both the policyholder and the third party if the driver was legally intoxicated.

However, if your voluntary insurance (first-class policy) denies payment, your compulsory insurance (Por Ror Bor) will still cover bodily injury to the other party regardless of intoxication, lack of license, or other traffic violations.

But compulsory insurance only covers injuries, not vehicle damage. You’ll still be personally liable for damage to the other car.

So the best advice? Don’t drink and drive. It’s not just illegal, it can cost you your safety, your money, and your peace of mind.

If Talking to Your Insurer Is Hard. Talk to Us Instead

Some insurers are clever at dodging responsibility. They claim things like “You must have been drunk before the test” or use made-up formulas to deny your claim.

If you’ve been hit with this “backdated alcohol” excuse don’t fall for it, and don’t fight alone.

📍 Contact Wongsakorn Law Office, led by Lawyer Arm, a legal expert specializing in car insurance and accident disputes.

We’re here to protect your rights, fight unfair insurance denials, and make sure you get the justice and compensation you deserve.