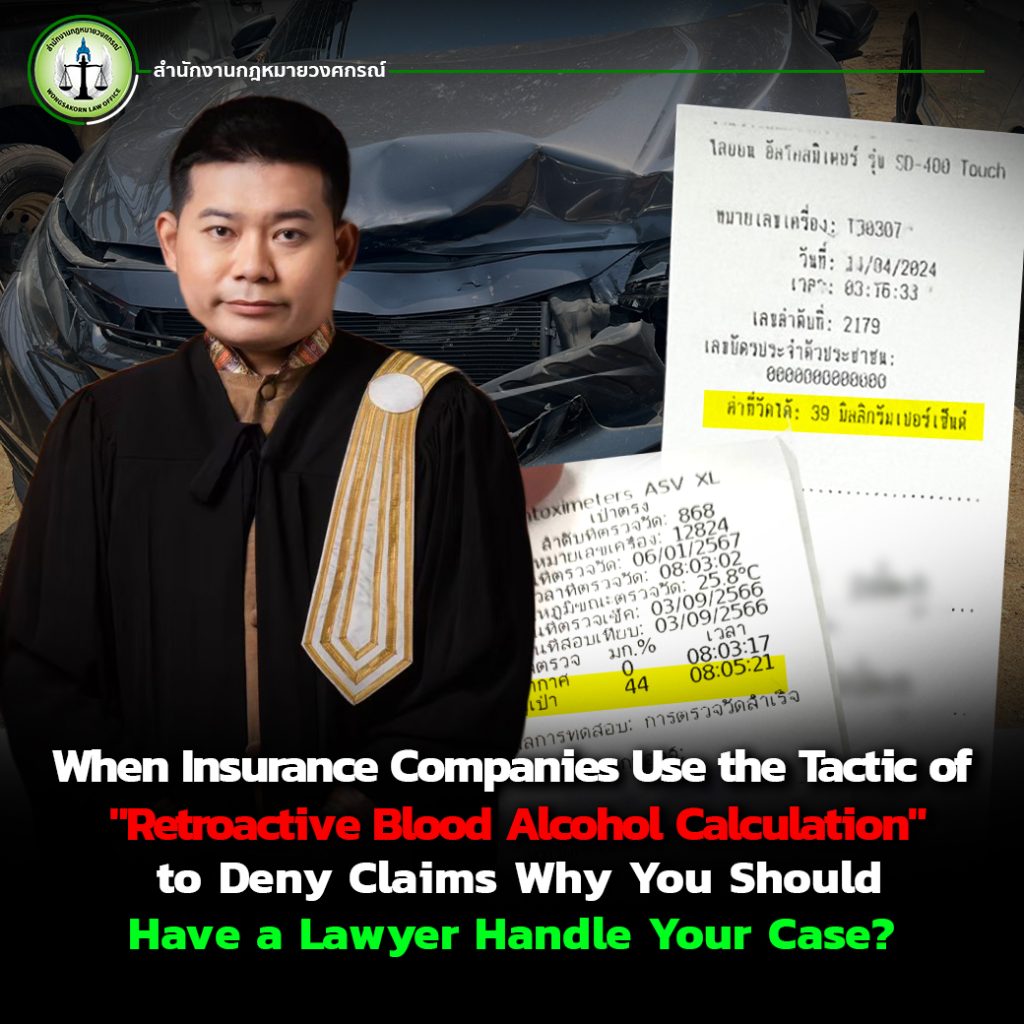

One of the common strategies used by many insurance companies to avoid paying compensation to policyholders is by claiming a retroactive blood alcohol level, even when the insured driver was not over the legal alcohol limit at the time of driving. This issue is highly controversial and has led to many disputes, causing prolonged hardship and damage to numerous victims or insured parties.

This often leads to confusion among victims Who question: If the breathalyzer test shows a blood alcohol content below 50 milligrams percent as allowed by law. Why does the insurance company still deny liability? And why is it better to let an experienced insurance litigation lawyer handle the process instead of managing it yourself?

This article from Wongsakorn Law Office aims to answer these questions by providing clarity and showcasing real case studies.

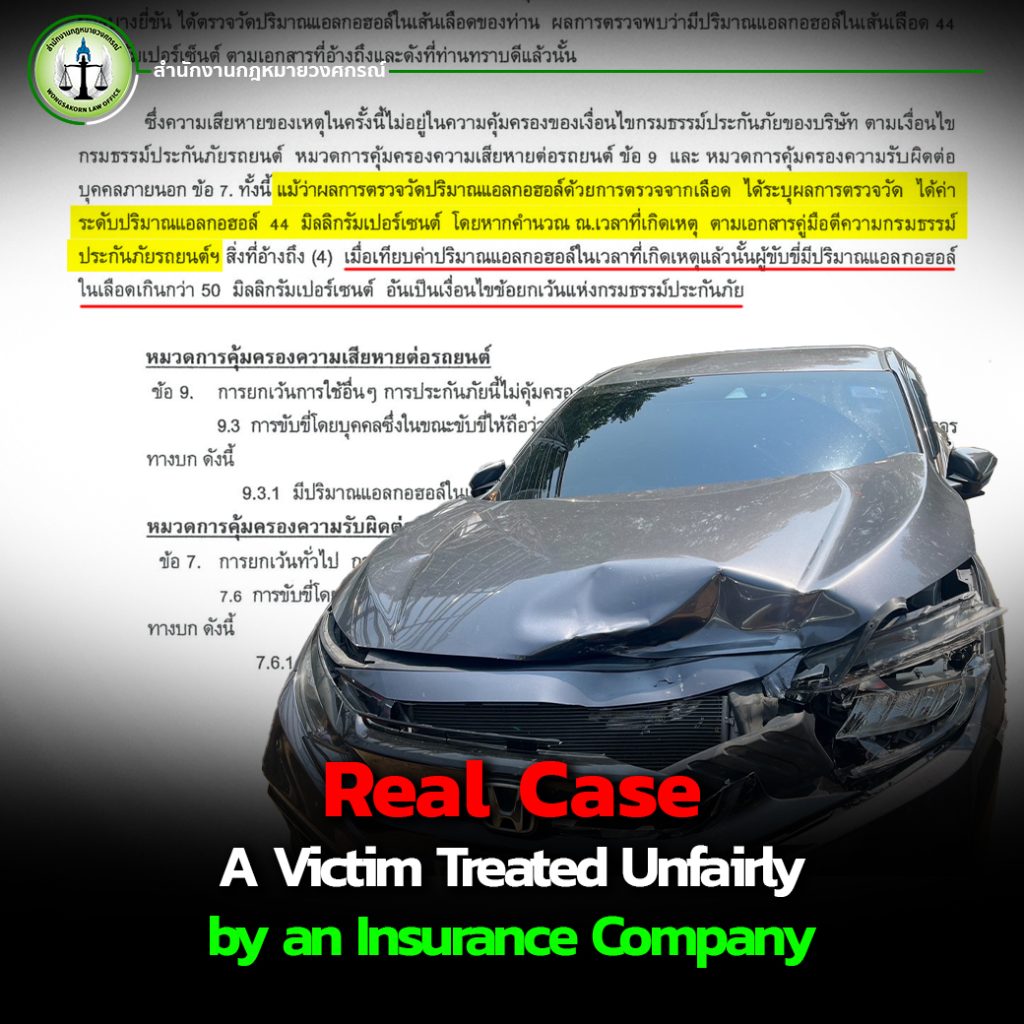

Real Case: A Victim Treated Unfairly by an Insurance Company

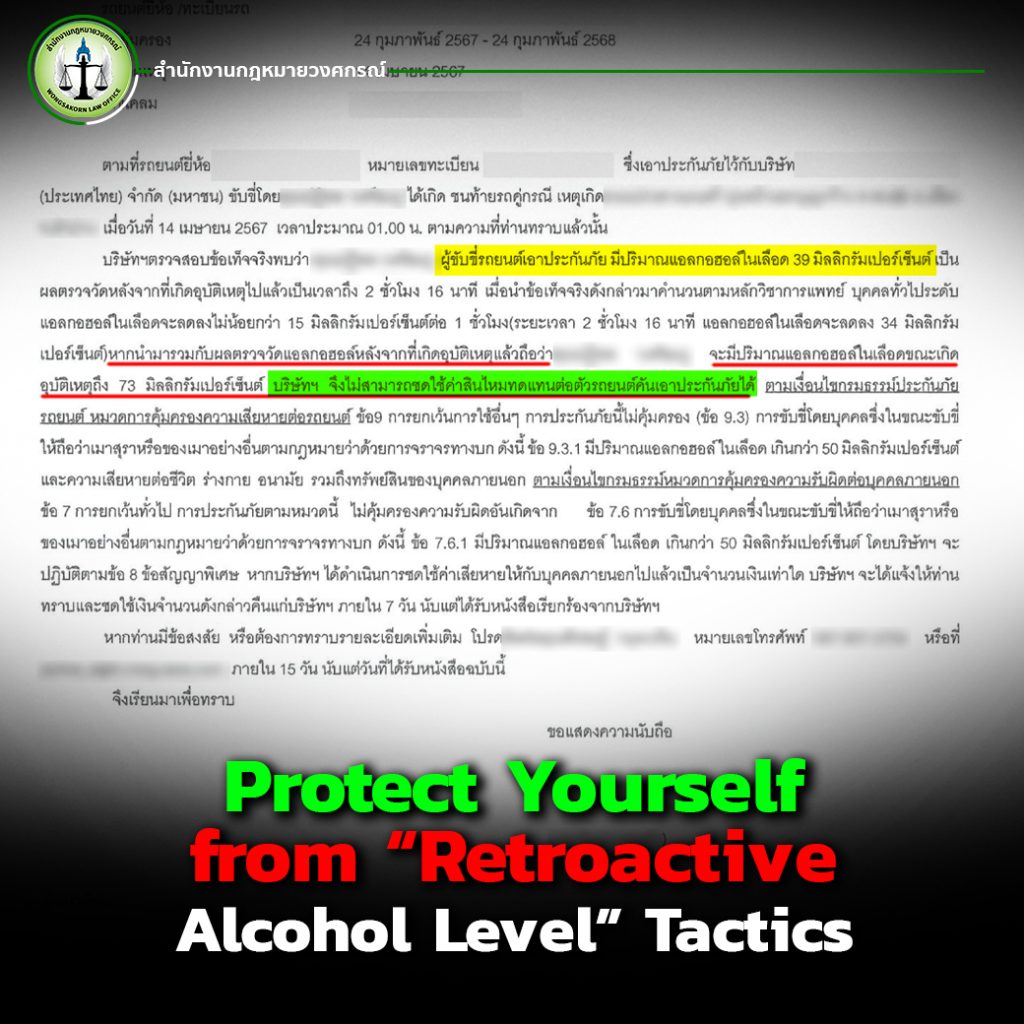

In this case, our client experienced an accident and admitted to consuming a small amount of alcohol—but not exceeding the legal limit. At the scene, the driver cooperated fully and took a breathalyzer test, which confirmed a result under 50 mg%, within legal limits.

Yet, the insurance company exploited a legal gray area. Despite the test result being legal, they refused to pay, citing “retroactive alcohol level calculation,” claiming that the driver’s BAC (blood alcohol content) must have been higher at the time of the accident. They made this assumption without any scientific or medical basis.

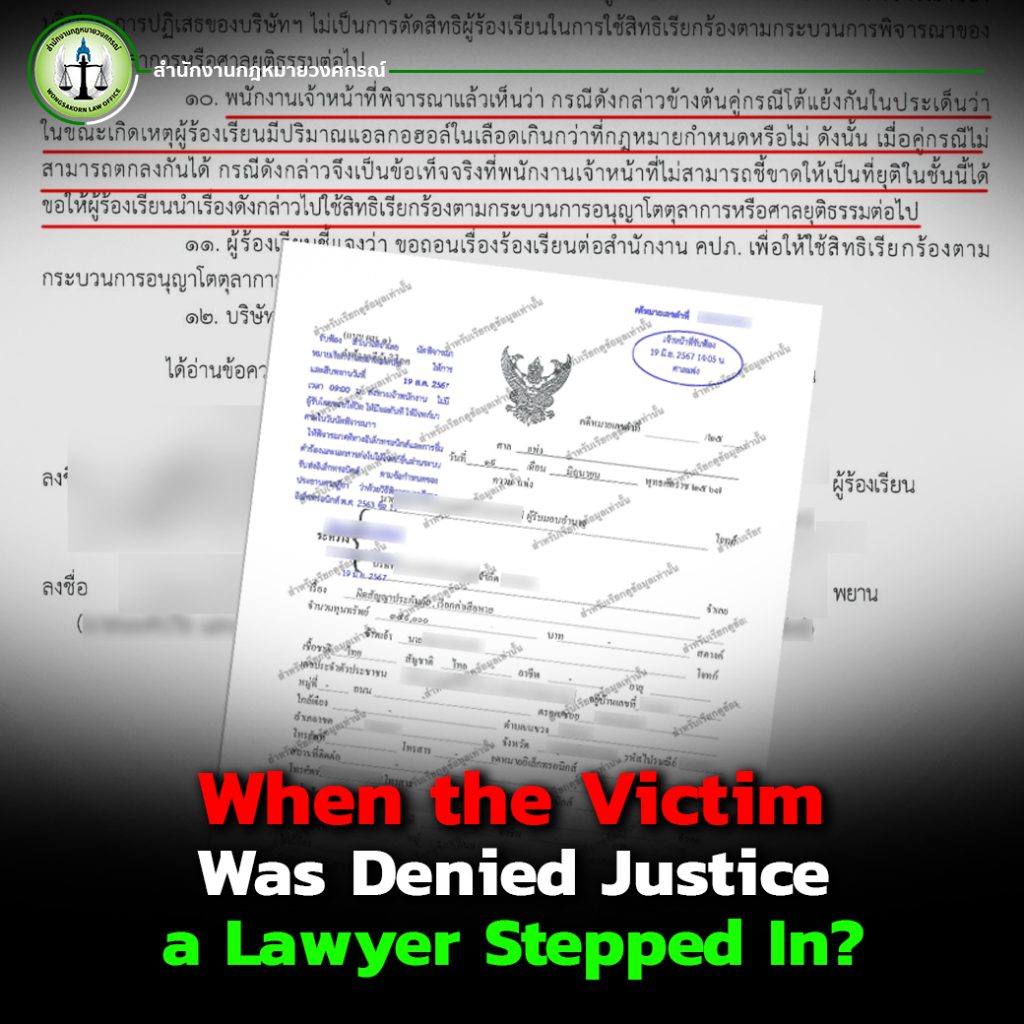

When the Victim Was Denied Justice, a Lawyer Stepped In?

The client assigned Wongsakorn Law Office to handle the case. We started by sending a formal Notice to the insurer. Still, they denied responsibility using the same flawed reasoning.

We escalated the issue to the Office of Insurance Commission (OIC), but OIC disappointingly replied that they had no authority to settle the dispute, leaving victims without reliable government recourse.

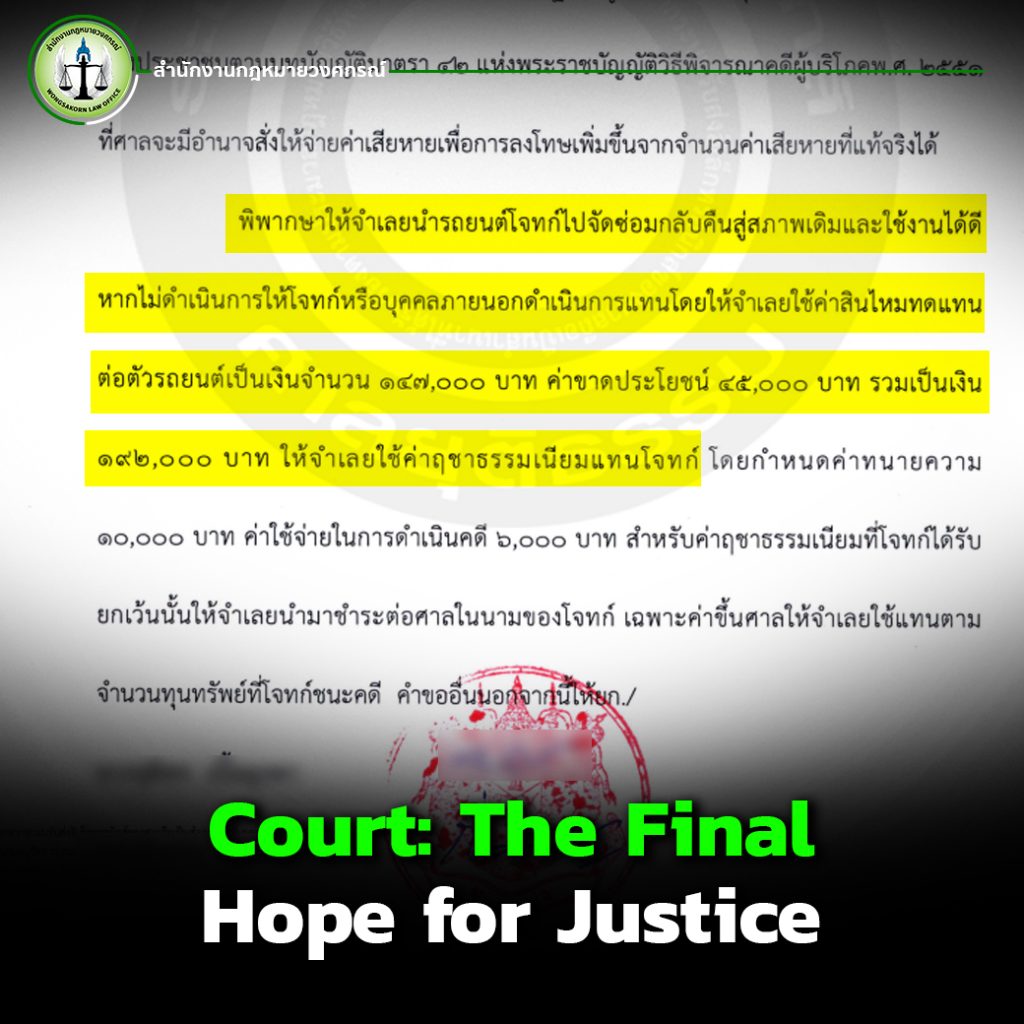

Court: The Final Hope for Justice

With no help from regulatory bodies, we filed the case in court. After thorough examination of the evidence and witness testimonies, the court ruled that the insurance company must pay compensation.

The judgment made it clear: retroactive alcohol calculation is not scientifically valid and cannot be used as a legal defense.

Why Is This Tactic a Dangerous Trap?

Many don’t realize that retroactive alcohol calculation is a common tactic among insurers. Our law firm has seen nearly every company use this to deny claims especially when victims don’t have legal counsel.

Without a lawyer, many victims give up their rights unknowingly and suffer unnecessary losses.

Which Companies Use This Tactic?

Sadly, almost all insurance companies have used this technique when they see that victims lack legal support. It’s a way to reduce company risk while unfairly shifting the burden onto customers.

Without a lawyer, policyholders are at the mercy of the insurer, with no checks or balances.

Protect Yourself from “Retroactive Alcohol Level” Tactics

If the victim in this case didn’t have a lawyer, the result might have been unjust even though the truth was on their side. That’s why having a legal expert on your side isn’t just about claiming rights, it’s about protecting them.

Don’t let this tactic become a systematic tool for companies to avoid payouts. Be informed, and get proper legal help when needed.

Talk to a Lawyer Now if You’ve Been a Victim of Retroactive Alcohol Claims

Car insurance shouldn’t just give you peace of mind, it should come with awareness of insurer strategies. If you or someone you know is facing denial of a claim based on this tactic, don’t delay. Consult with a lawyer.

The legal team at Wongsakorn Law Office has direct experience handling insurance disputes and is ready to protect your legal rights. If you need help with a case involving “retroactive alcohol calculations,” click to contact us.