DUI cases no driver ever wants to face one, especially when they truly weren’t drunk. Unfortunately, that wish rarely aligns with reality. Nowadays, when an accident occurs, drivers are often quickly accused of driving under the influence.

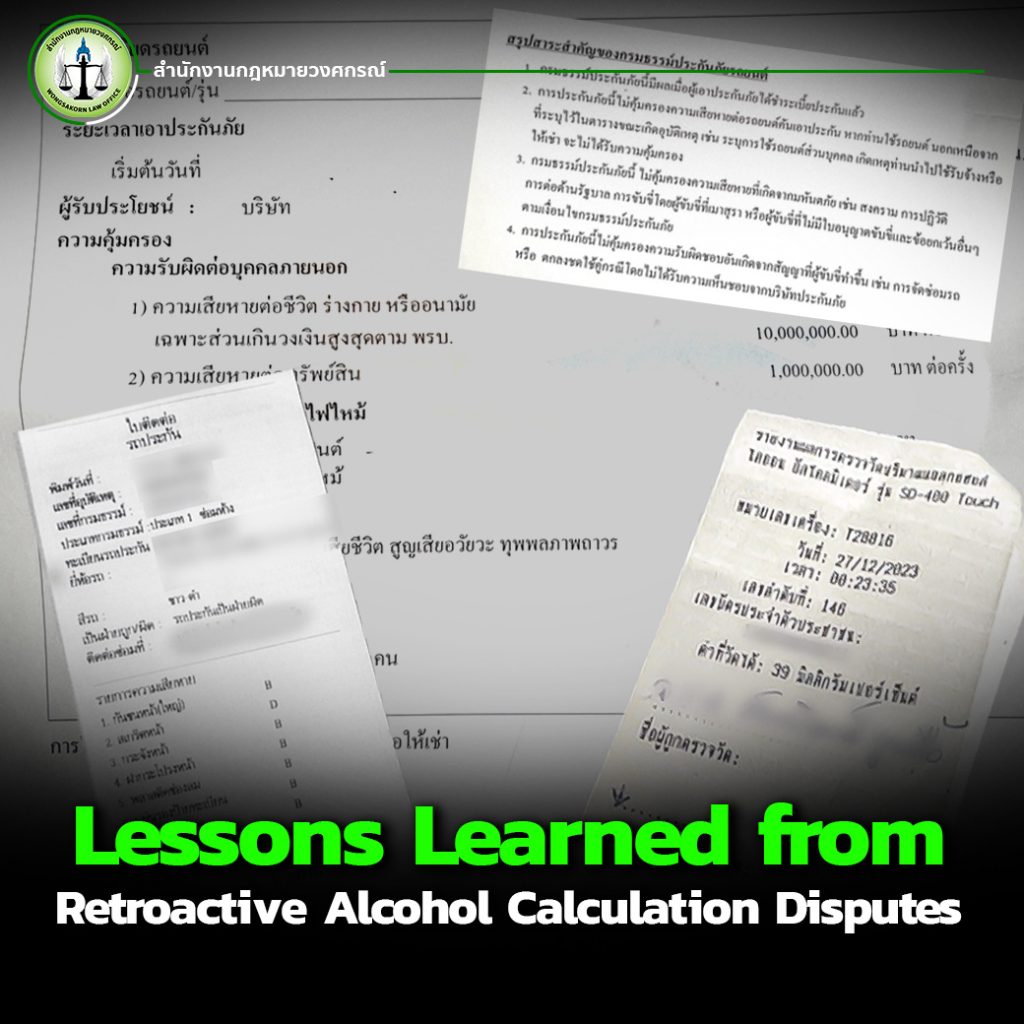

Insurance companies frequently manipulate “retrospective alcohol calculations”, inflating the driver’s blood alcohol level beyond the 50 mg.% legal limit and then refusing to compensate for damages.

At Wongsakorn Law Office, approximately 90% of DUI clients we handle were unfairly accused because insurers retroactively calculated alcohol levels. Even when drivers insist they weren’t drunk, once the reading exceeds 50 mg%, insurance companies automatically deny coverage leaving the driver to face both criminal charges and financial loss.

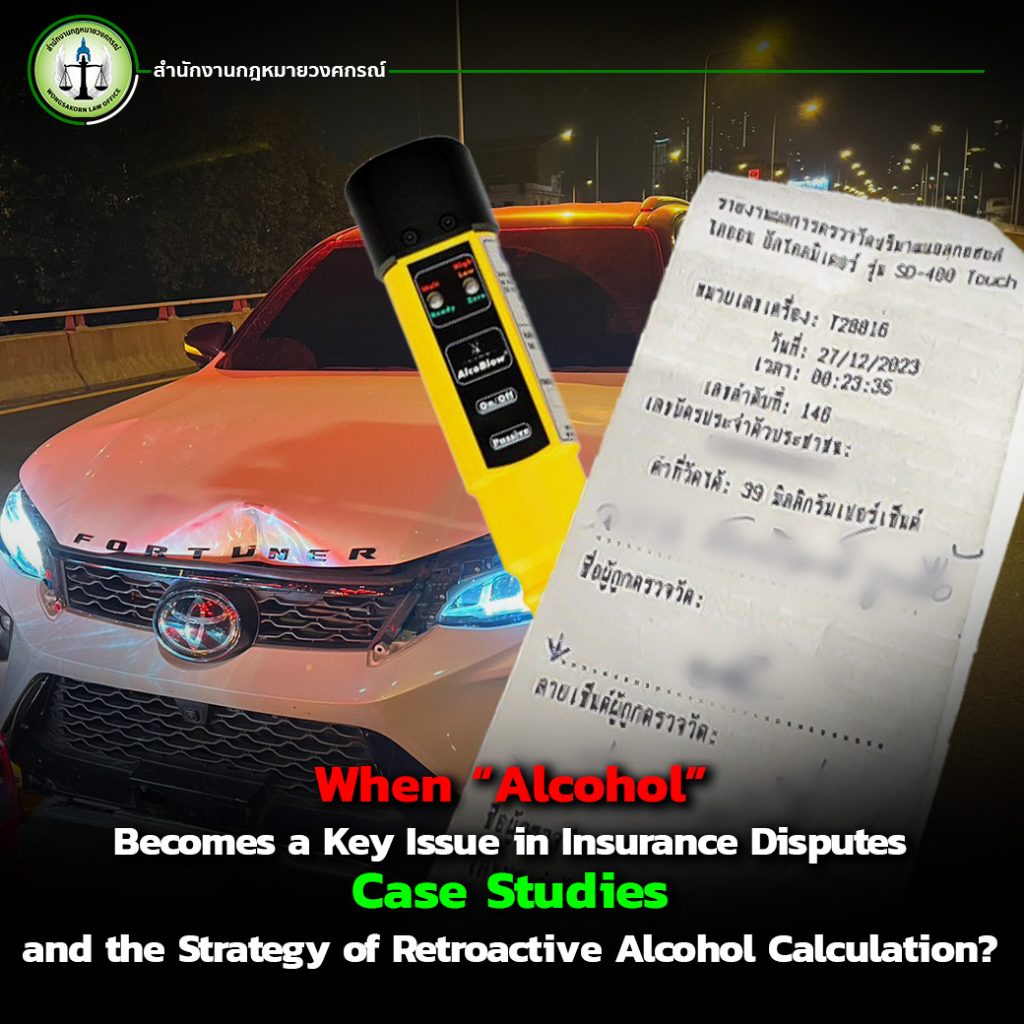

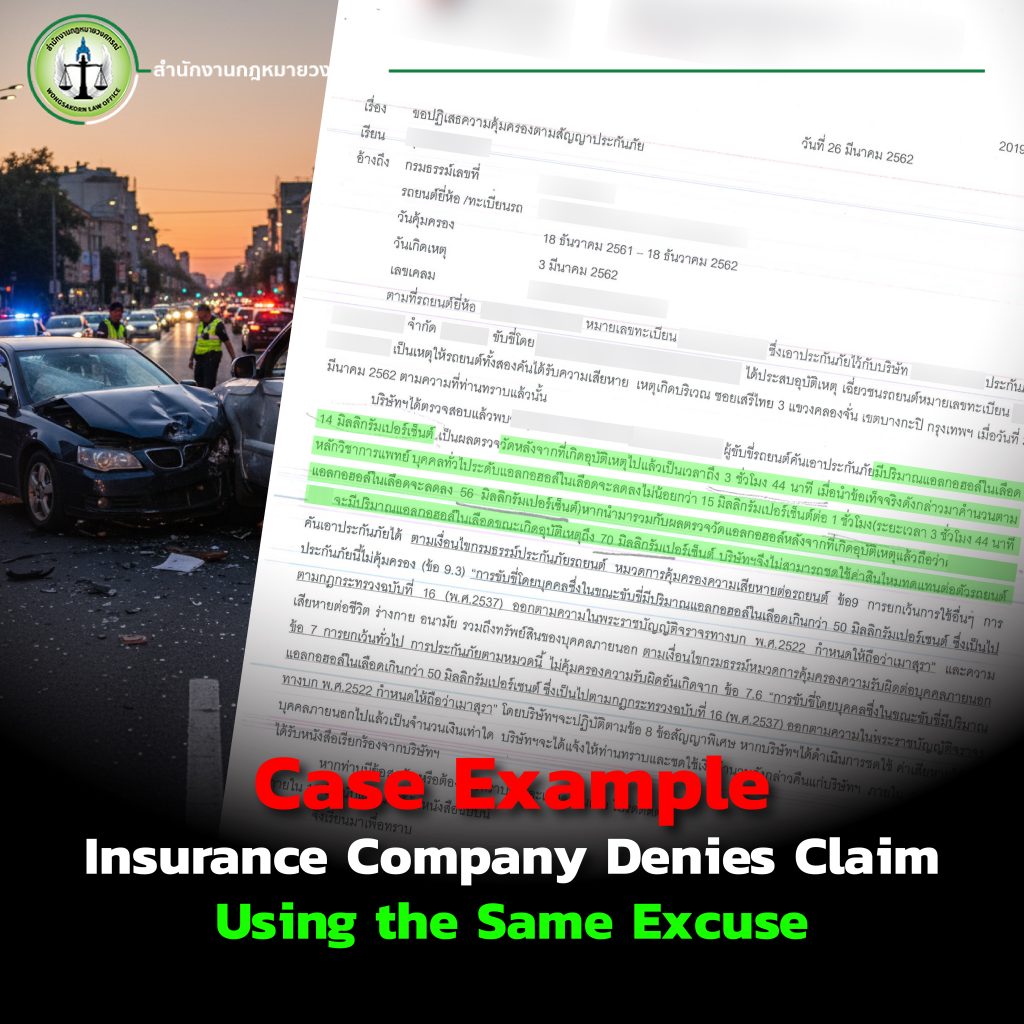

Case Example: Insurance Company Denies Claim Using the Same Excuse

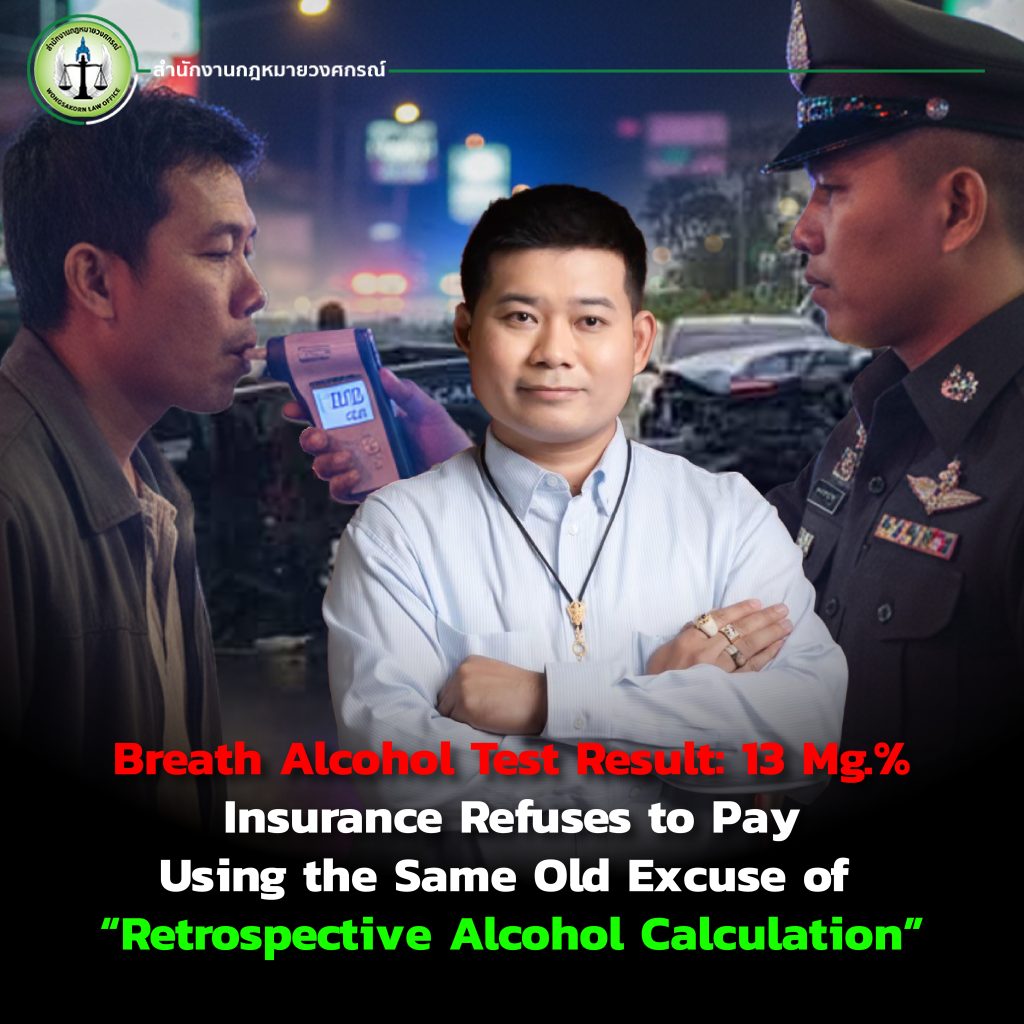

In this case, the victim had a breath alcohol test result of only 13 Mg.% immediately after the accident. Despite this, the insurance company refused to cover any damages, falsely claiming that the actual alcohol level exceeded 50 Mg.%.

Feeling that this was unfair, the victim filed a complaint with the Office of Insurance Commission (OIC). However, the insurer stood firm and continued to deny responsibility. Exhausted and frustrated, the victim turned to Lawyer Arm, a legal expert in automotive insurance law, who took the case and successfully pursued compensation for the client.

Our office strongly advises victims not to face such cases alone. Consulting a lawyer ensures you’re protected from unfair settlements and the emotional toll of dealing with a DUI accusation especially when you weren’t at fault.

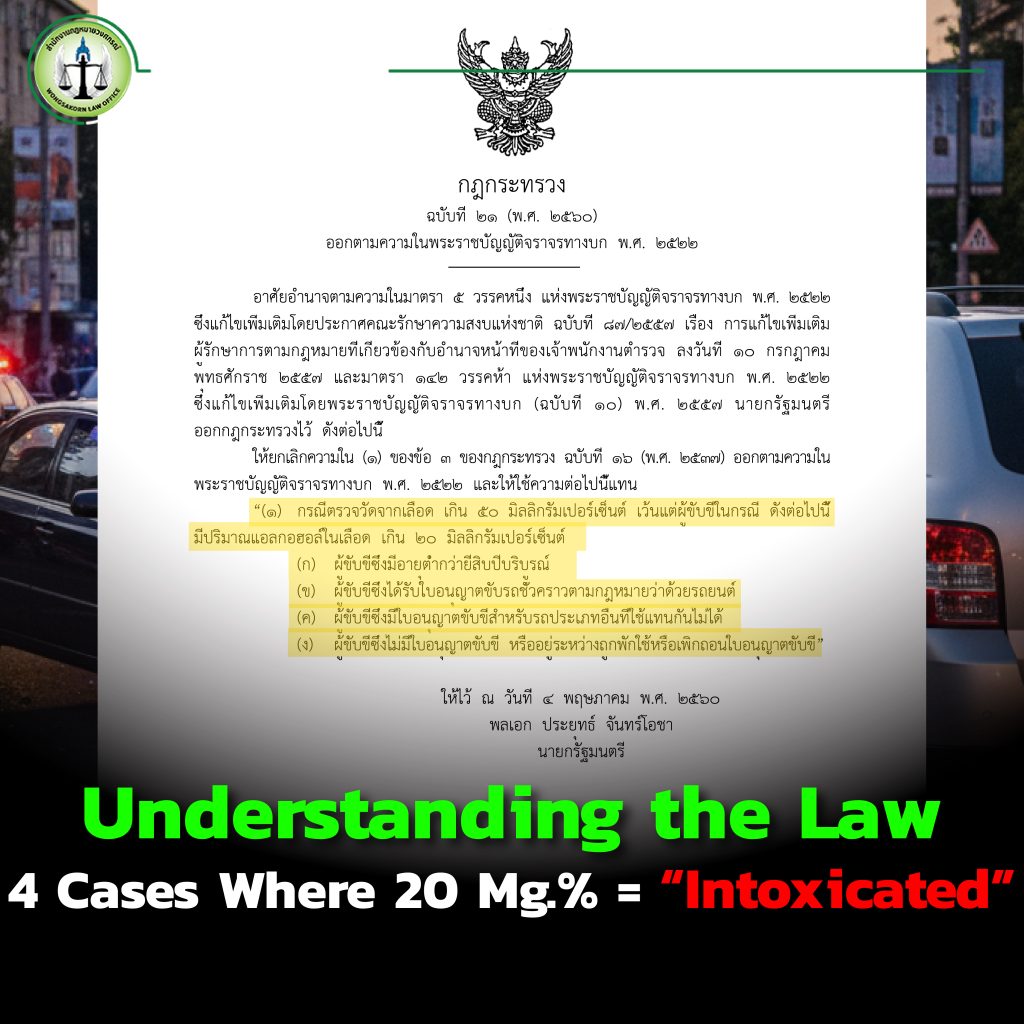

Understanding the Law: 4 Cases Where 20 Mg.% = “Intoxicated”

According to the Ministerial Regulation No. 21 (B.E. 2550) under the Land Traffic Act B.E. 2522, a blood alcohol concentration exceeding 50 Mg.% is legally considered intoxicated.

However, in the following four cases, exceeding 20 Mg.% is already considered “drunk”:

1. Drivers under 20 years old

2. Drivers with a temporary license (2-year license)

3. Drivers holding a license of a different category

4. Drivers with revoked or suspended licenses

While the new traffic laws (2023 revision) clearly define these limits, the most effective prevention remains simple: do not drink before driving. Compliance with traffic laws and awareness of alcohol effects will greatly reduce DUI cases and accidents.

DUI Cases – A Common Legal Battle

DUI insurance disputes are among the most frequent cases we receive. Despite being featured on high-profile media such as #HoneKrasae, insurance companies continue using unfair tactics notably retrospective alcohol calculations to evade payment.

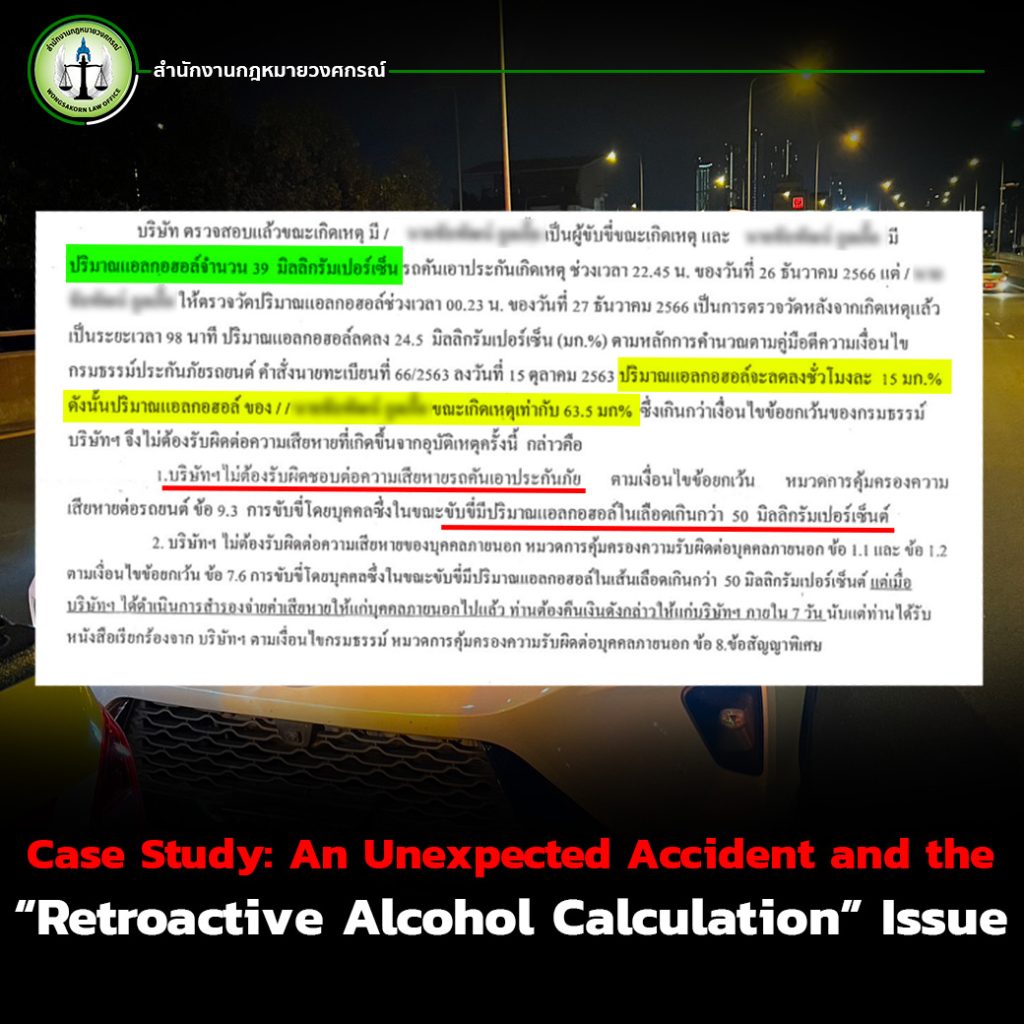

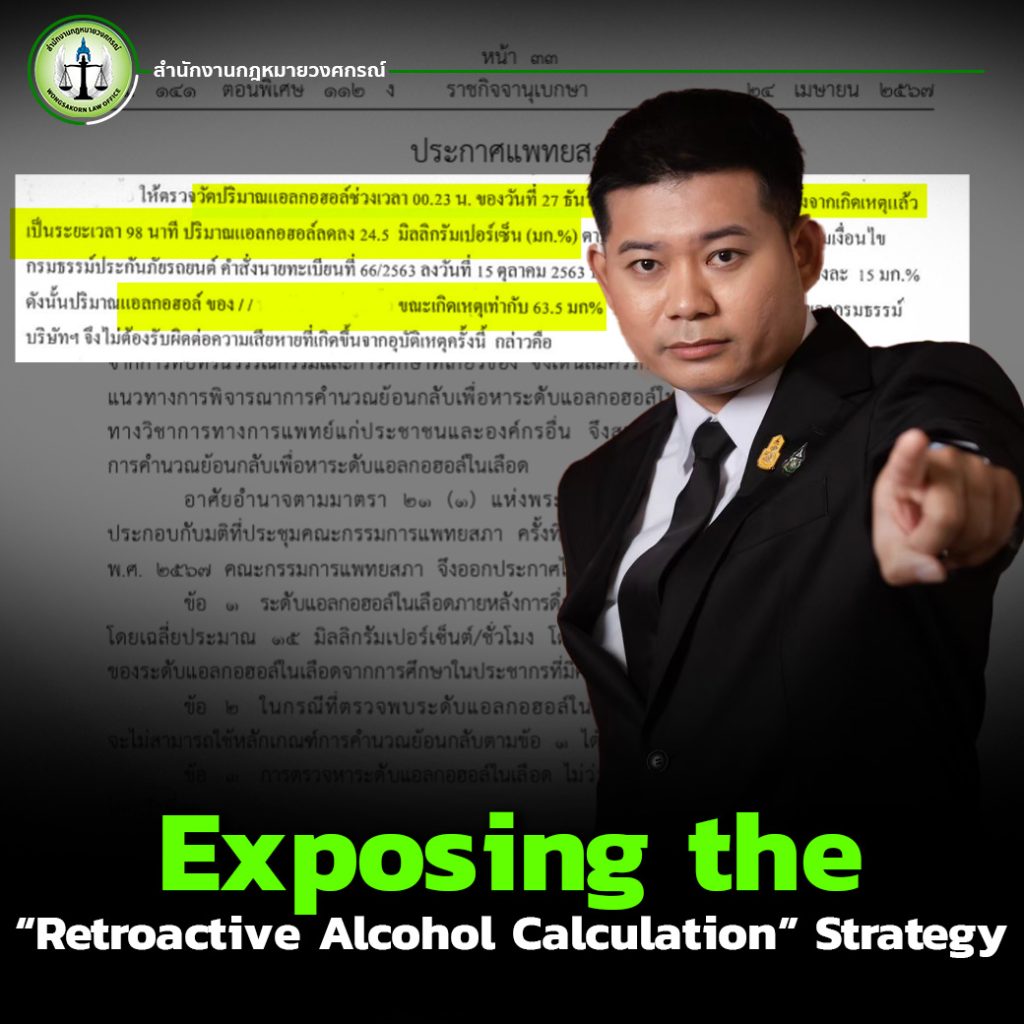

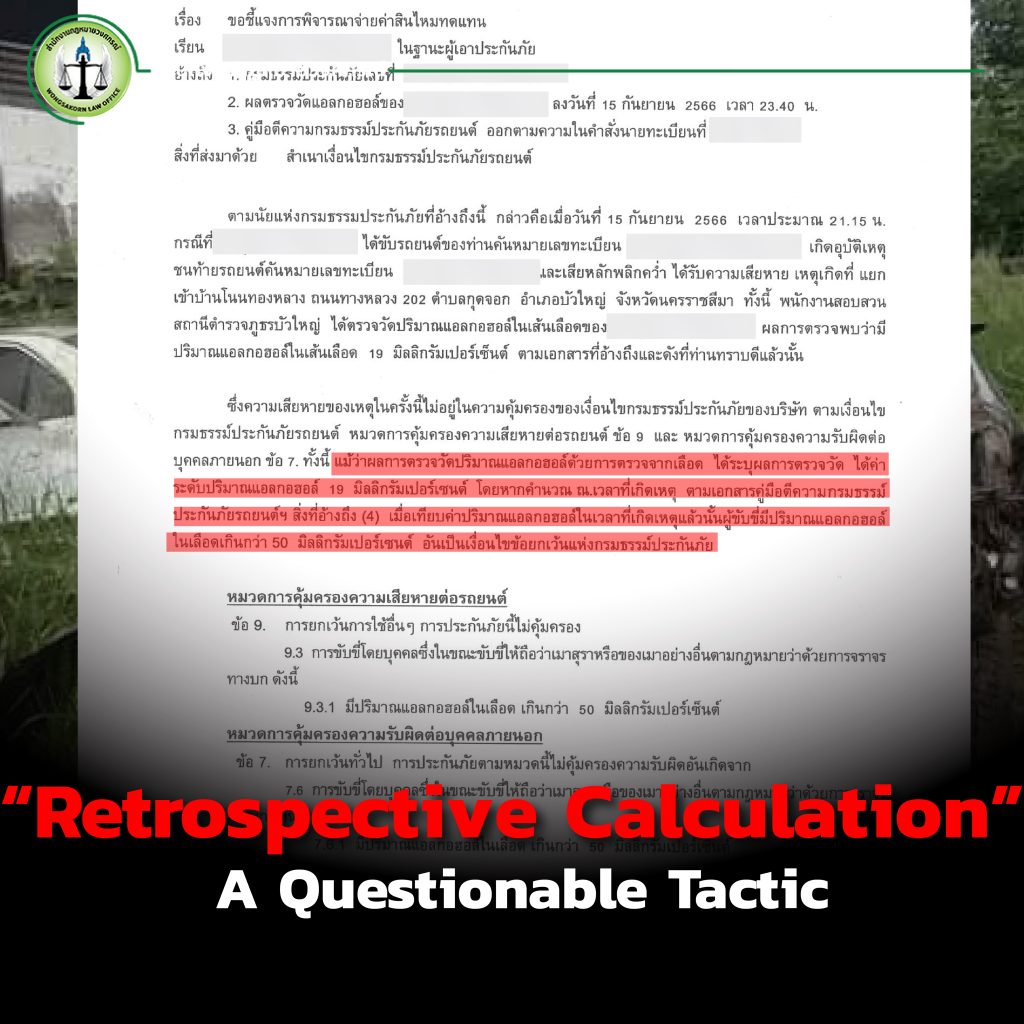

“Retrospective Calculation” A Questionable Tactic

This tactic involves delaying alcohol testing after the accident, then using the theory that alcohol levels drop by 15 Mg.% per hour to estimate a higher concentration at the time of the accident.

This manipulation has drawn many consumer complaints, as it’s clearly unfair and exploitative toward victims who were not intoxicated.

Many clients find themselves accused of DUI even without drinking at all, labeled as “drunk drivers” with alleged readings above 50 mg%. Such conduct not only harms victims financially but also damages their dignity and trust in the insurance system.

Ultimately, many victims who never intended to file lawsuits end up having to do so simply because insurance companies refuse to take responsibility from the start.

Legal Advice from Wongsakorn Law Office

If you’re in a similar situation where your insurer uses retrospective alcohol calculations to deny payment don’t waste time arguing or handling the claim yourself. Consult an experienced lawyer immediately.

You can reach out to the Lawyer Arm or contact Wongsakorn Law Office directly through our official page, “Law & Motor Insurance.”