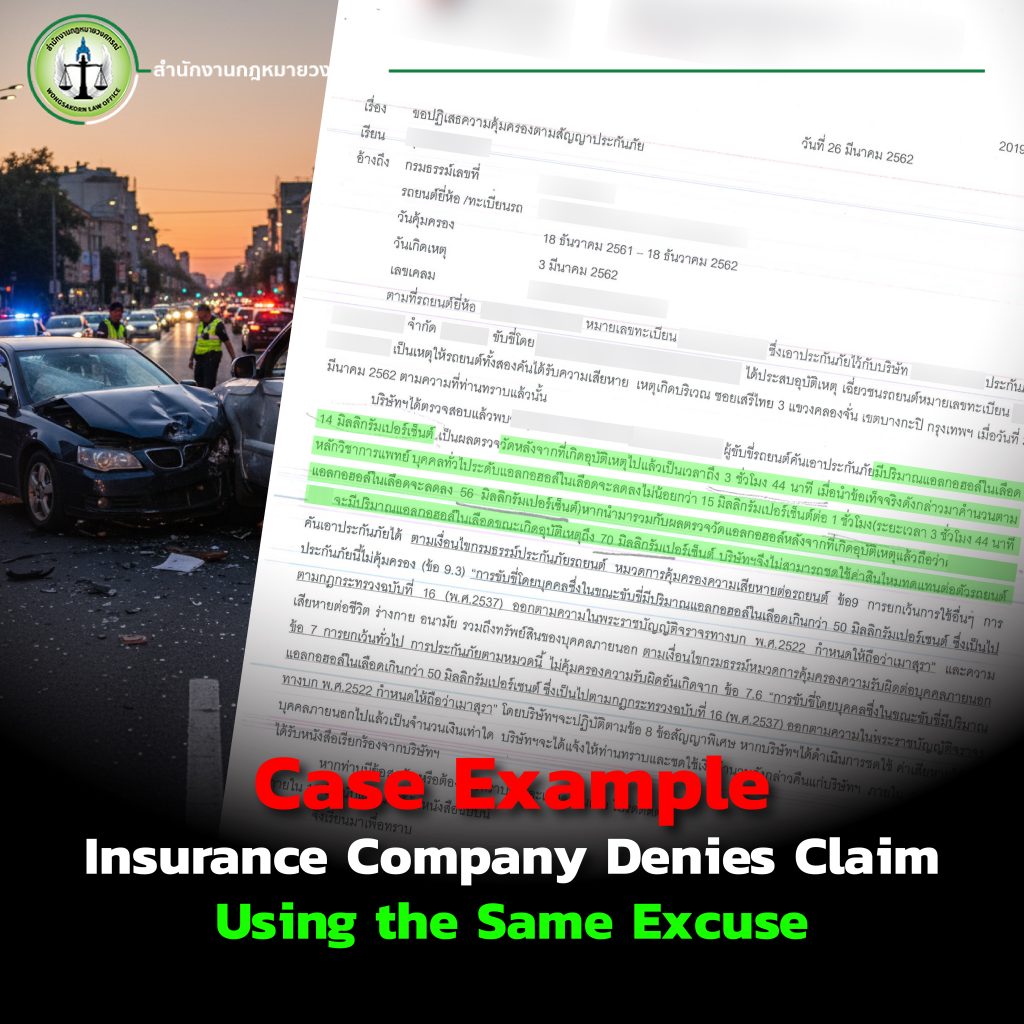

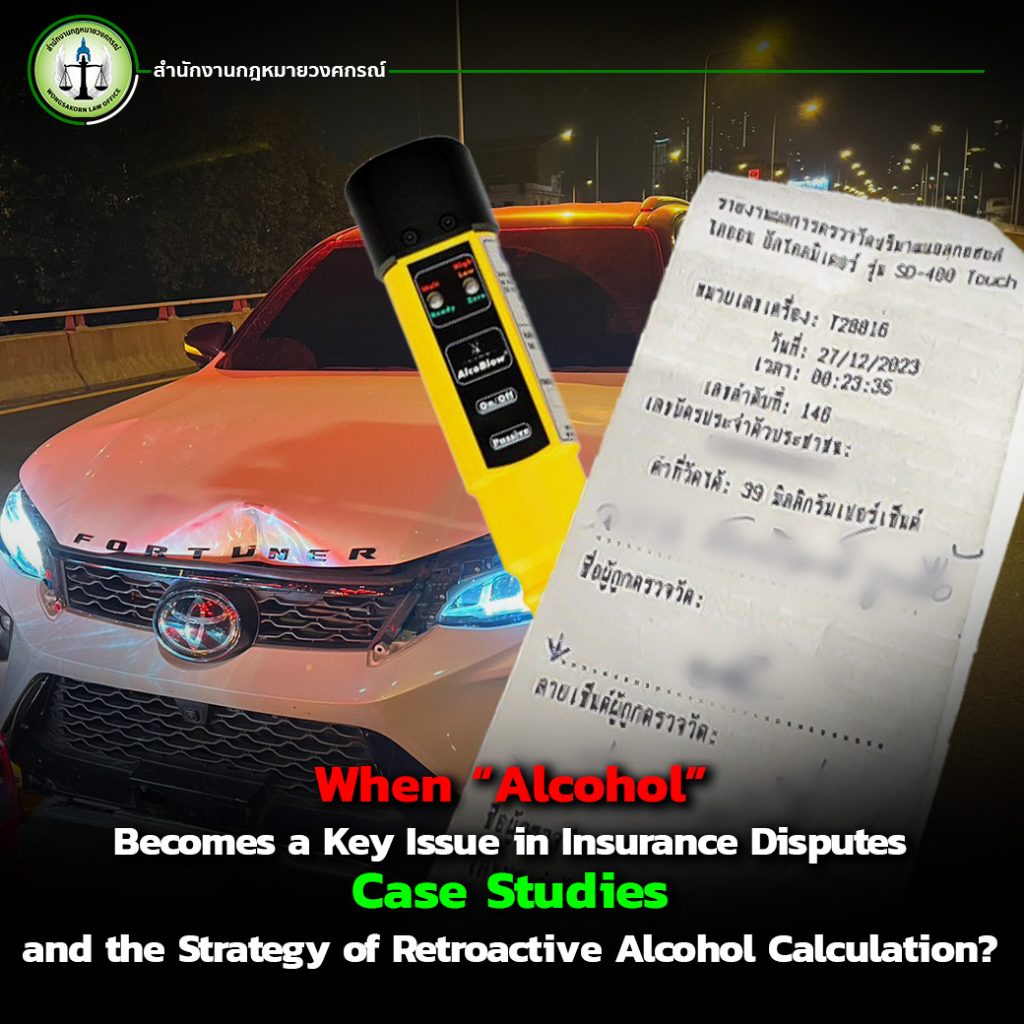

Alcohol exceeding 50 milligrams percent while driving becomes a major point of conflict between victims and insurance companies. When a road accident occurs, one of the issues that is always raised for consideration is the “back-calculation of blood alcohol content” of the driver, especially in cases involving insurance claims. Many people may have encountered situations like this.

The key question is: Is this kind of alcohol back-calculation fair to consumers?

This article from Wongsakorn Law Office will take you deeper into the issue of alcohol and insurance, explaining mechanisms that many people may have never known before.

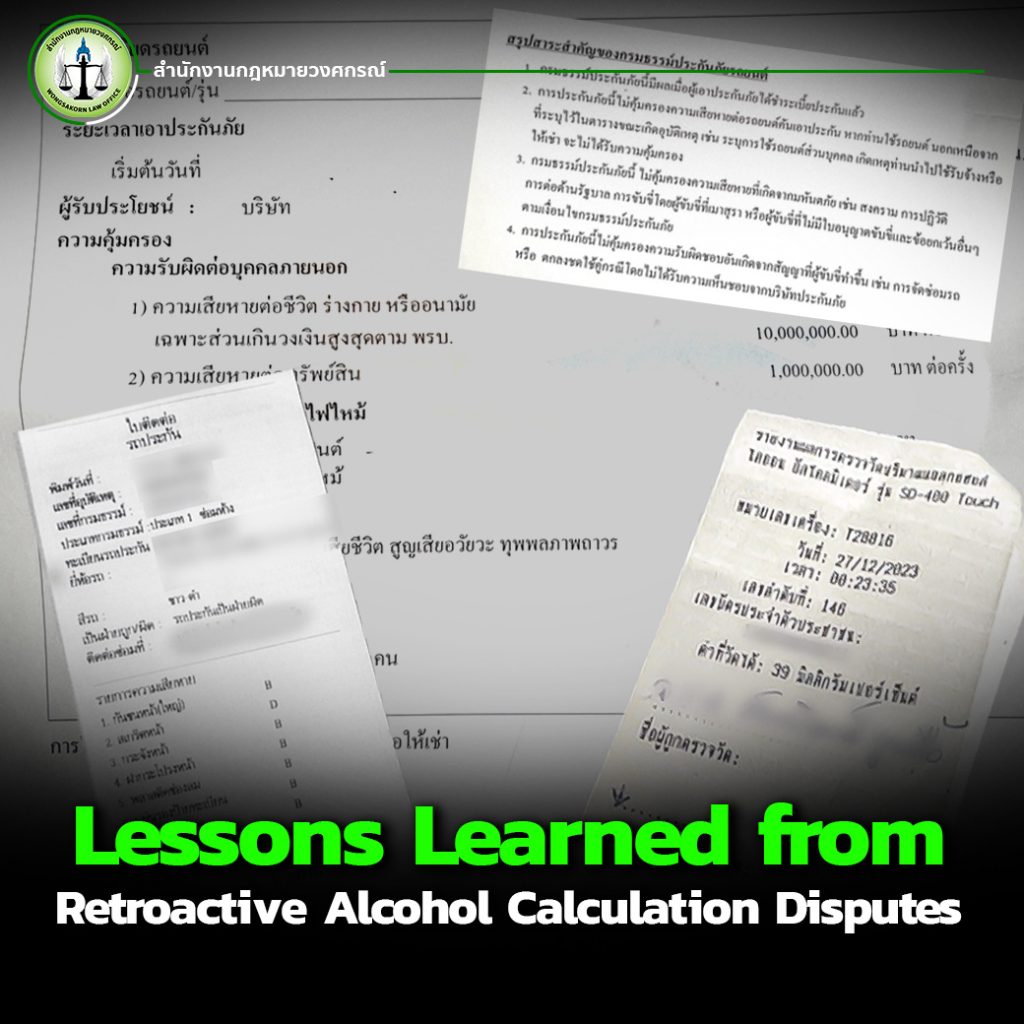

Conditions in insurance contracts regarding alcohol

In general, motor insurance policies clearly state an important condition:

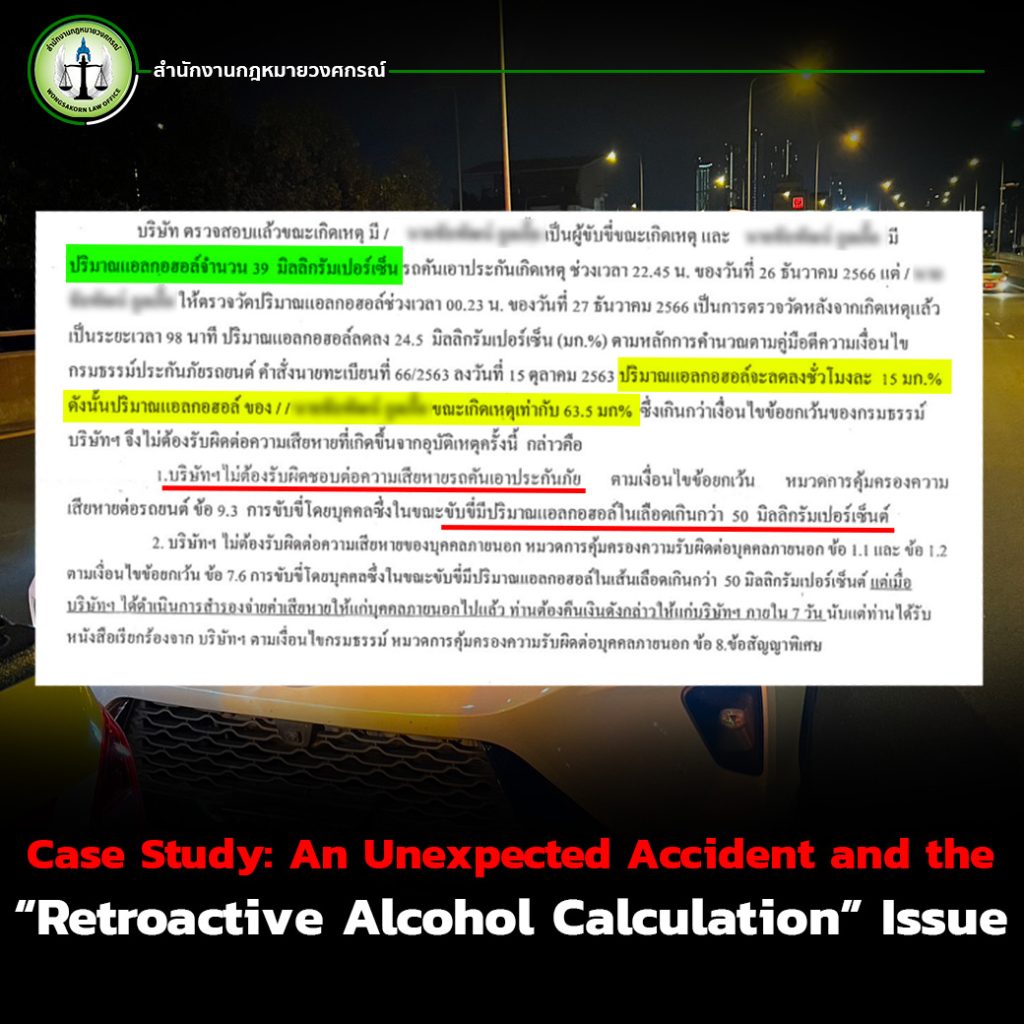

The company will not pay compensation if the driver’s blood alcohol level exceeds 50 milligrams percent “while driving.”

It sounds straightforward, but in practice there is a significant “gap,”

because the term “while driving” cannot be measured in real time.

The starting point of the issue of alcohol back-calculation

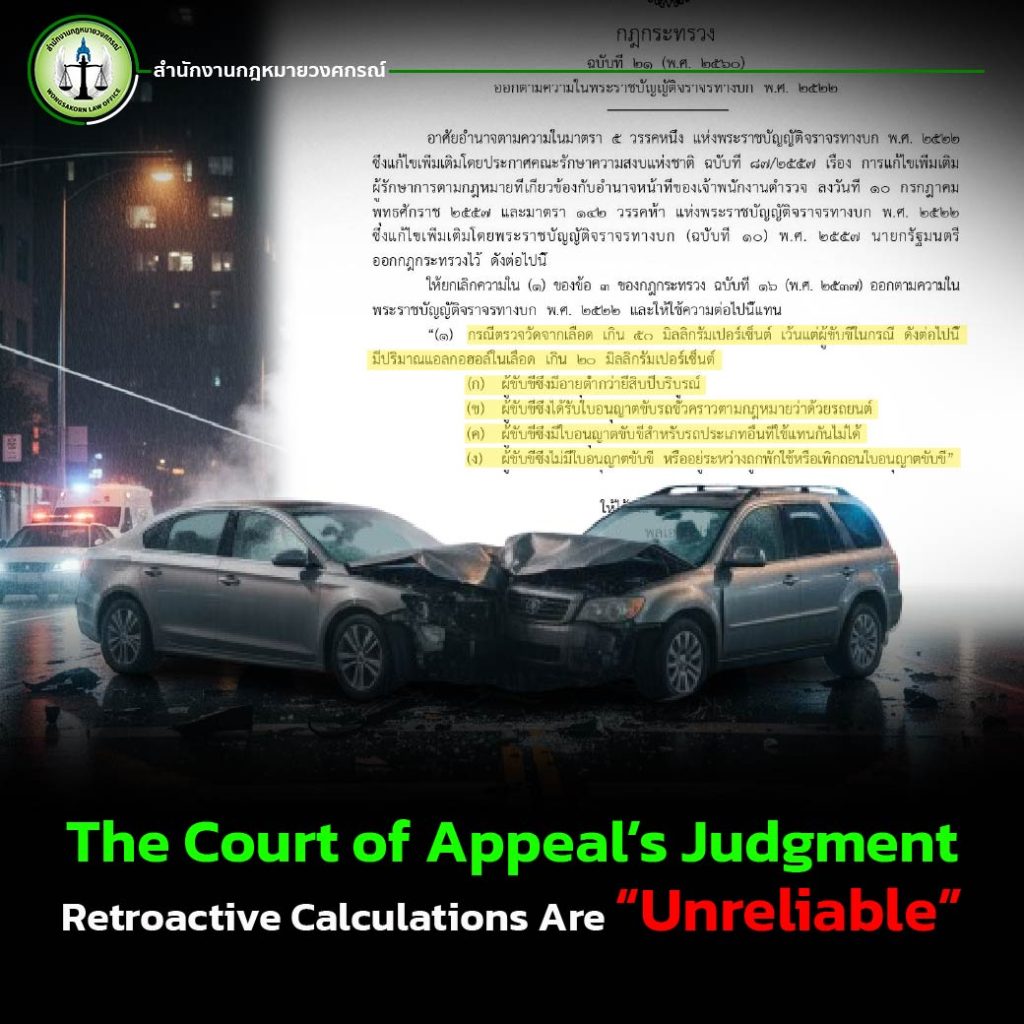

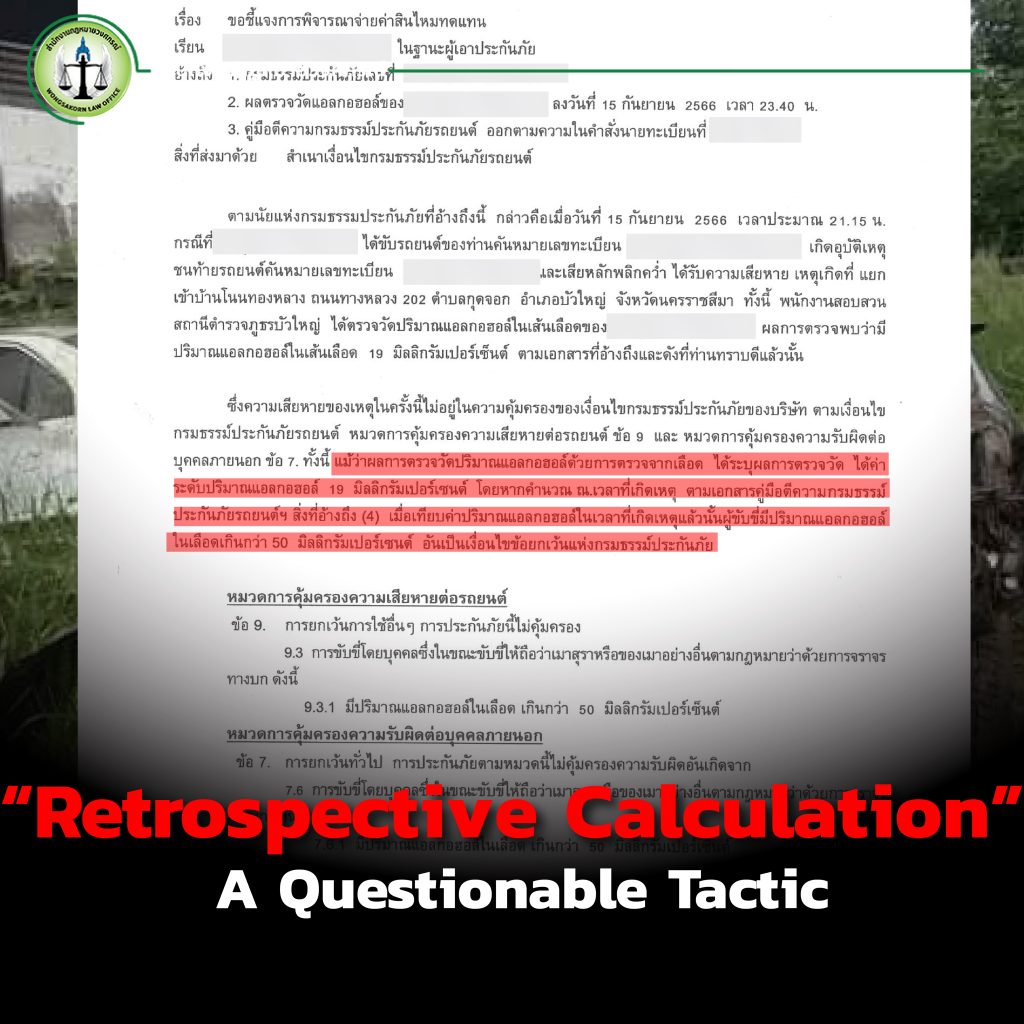

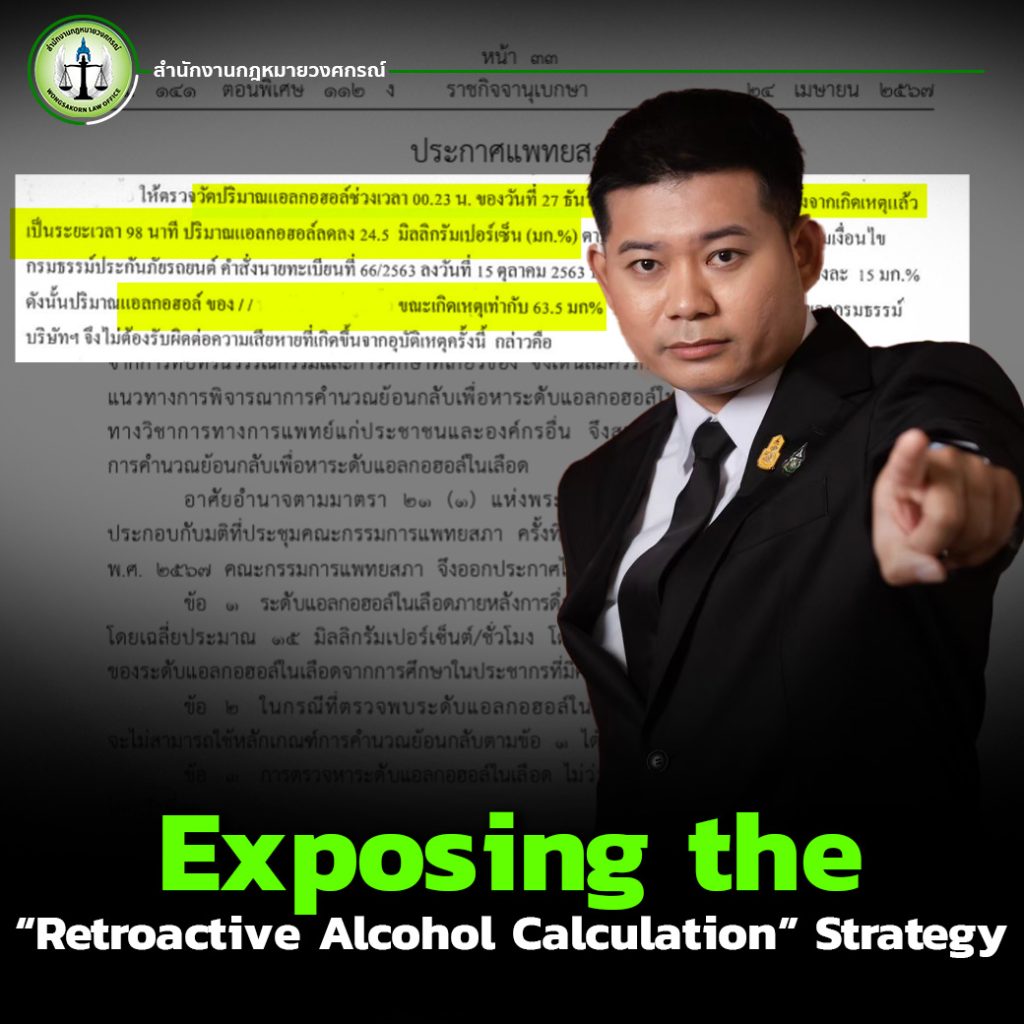

In reality, when an accident occurs, alcohol testing usually takes place “after the incident.” This leads to the concept of “alcohol back-calculation,” which is a medical principle used to calculate backward from the level detected at a later time.

So who determines that “back-calculation” should be used?

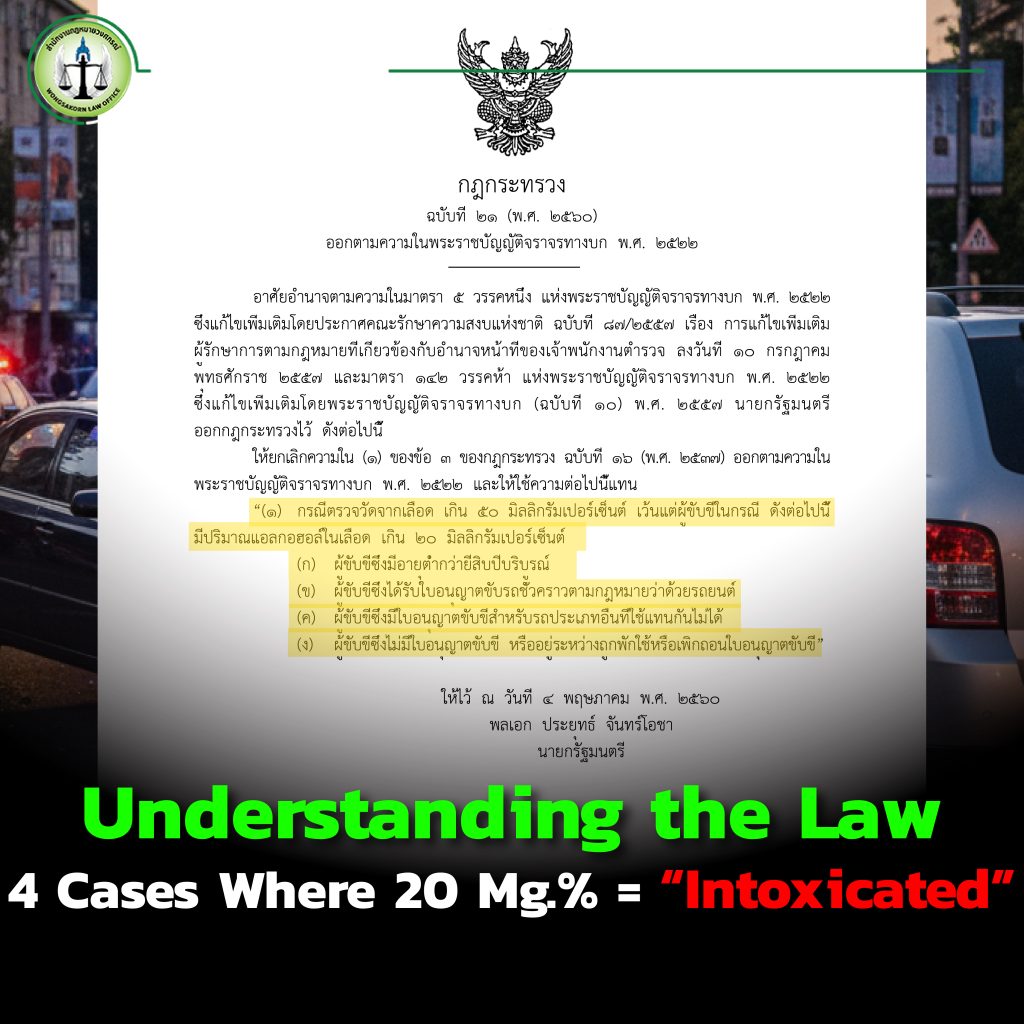

There are guidelines from regulatory authorities that allow back-calculation in certain cases, such as using the rate of alcohol metabolism in the body.

But the problem is that the general public has little to no knowledge about this.

Why do victims feel they are being “treated unfairly”?

Try to imagine this situation:

- You did not feel intoxicated while driving.

There was no explanation about back-calculation when purchasing the insurance.

But after the incident, the insurance company uses “back-calculation”

and concludes that your alcohol level exceeded the limit while driving.

The result is that your claim is immediately denied afterward.

Can this be called “tricky” or “cunning” insurance?

From the victim’s perspective, many people see it as the use of technical or legal loopholes, because it was never explained at the time of purchase that alcohol back-calculation would be applied while driving; it relies on medical principles that are difficult to understand, as not every member of the public can grasp such concepts; and it is often used at the moment of “denying payment.” When it is found that the driver had alcohol in their system while driving, the insurance company uses this approach to immediately deny the claim, in order to protect its own interests, rejecting first in the hope that the victim will believe it. If the victim believes it, the company does not have to pay any compensation.

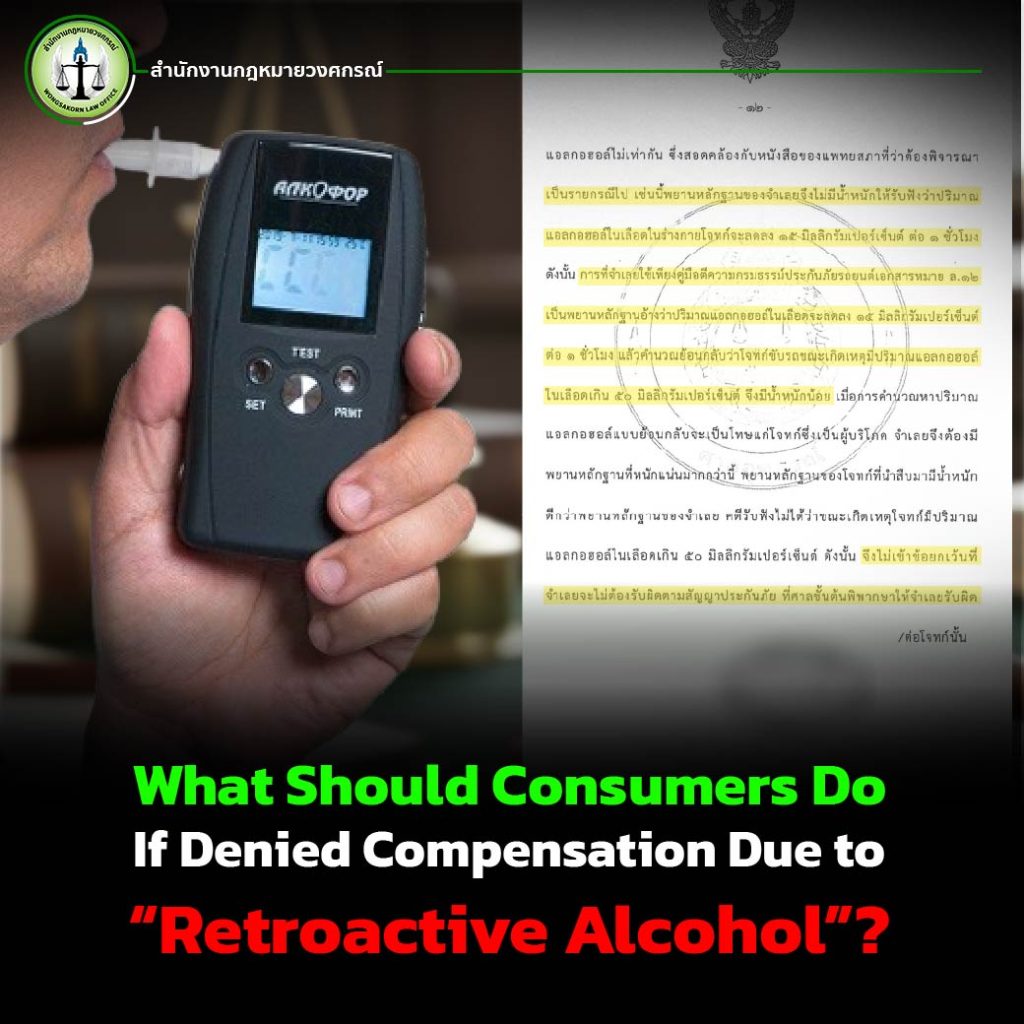

The truth that must be understood Back-calculation is not a 100% conclusion.

What is important for victims to know is

Alcohol back-calculation does not mean that at the time of driving, you always had a blood alcohol level exceeding 50 mg.%

Because the level of alcohol in the body

depends on many factors, such as

the time of drinking,

the amount of food in the stomach,

body weight,

and each individual’s metabolism.

Therefore, back-calculation is only an “estimation,” not a 100% fixed fact.

A common strategy used by insurance companies

From experience in many insurance cases, one approach frequently used is

“Deny first if the victim does not dispute it, the matter ends.”

Why does this strategy work?

Because most victims do not know the law. Insurance companies use terminology and principles in a way that leads victims to believe they are actually at fault. Most people are reluctant to fight or dispute, as they do not want trouble or to go to court. This becomes a loophole that allows insurance companies to gain an advantage with minimal effort, because in the end, the company does not have to pay any compensation.

Do not immediately believe that you had “excess alcohol” without verification

The most dangerous thing is when a victim “immediately believes” that they are at fault,

when in reality, there may still be many legal arguments available.

Questions you should ask

- When was the alcohol test conducted?

- How much time had passed since the incident?

- How accurate is the back-calculation method?

- Are there other factors that could affect the measured value?

The best solution consult a lawyer immediately after the incident

If you or someone close to you has been involved in an accident and there is an issue regarding alcohol or alcohol back-calculation,

What you should do immediately is do not wait, do not assume, and do not immediately believe the insurance company.

Why is it necessary to consult a lawyer right away?

Because a case must be “structured” from the very beginning. Certain evidence or information must be collected immediately, and responding requires specialized knowledge.

Because insurance companies already have legal teams

What many people may not know is that insurance companies already have legal teams, litigation approaches, and negotiation strategies to persuade victims to settle, even from “before the incident” occurs.

Therefore, if a victim does not have an expert to handle the compensation claim process, they are clearly at a disadvantage.

Being subjected to alcohol back-calculation is not the end of your rights

Having an issue related to alcohol back-calculation does not mean you “lose your rights” immediately. What matters is that you stay informed and do not allow yourself to be taken advantage of by the insurance company.

If you are facing this problem

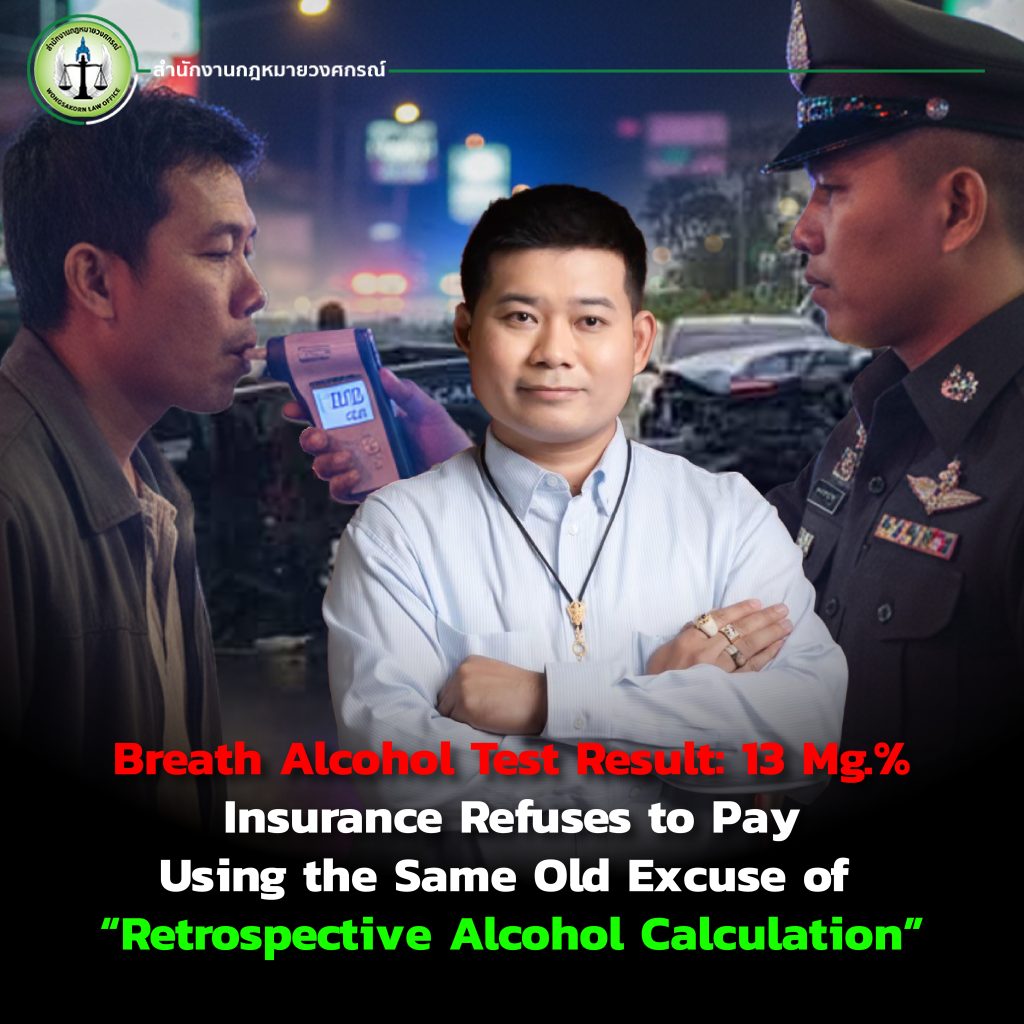

If your claim has been denied due to “alcohol back-calculation,”

do not let the matter end easily. In many cases our office has handled, there has not been a single case lost, because we pursued each case to the fullest extent. Victims can fight and claim their rights.

An option for those seeking fairness

Consulting a lawyer who specializes in insurance cases, especially those involving alcohol back-calculation, will help you understand your rights, plan your case correctly, and increase your chances of receiving fair compensation.

Do not let a lack of knowledge cause you to lose your rights.