Today, motor insurance is no longer something distant or a luxury. Instead, it has become a basic necessity for all vehicle users whether you drive to work, meet clients, travel to other provinces, or regularly rely on a car in your daily life. This is because life on the road is full of risks that are impossible to predict or completely avoid.

The purpose of motor insurance is simple and easy to understand: to protect against unforeseen risks, especially in situations where we are at fault in an accident and are unable to bear the resulting damages on our own. We never know how serious the consequences of an accident may be for the other party.

In some cases, the damage may only involve minor vehicle repairs. However, in other cases, the consequences may be severe, such as:

- The other party suffering serious injuries

- Permanent disability

- Or, in the worst-case scenario, loss of life

In addition, there may be damage to property, vehicles, buildings, or assets belonging to third parties. These damages can be far beyond what an average individual can afford. Therefore, motor insurance acts as a form of “protective armor,” helping to reduce financial burdens and providing protection for both drivers and victims.

Life on the Road Is Filled with Unavoidable Risks

An undeniable truth is that modern life is inherently risky:

- There is a risk that we may collide with others

- And a risk that others may collide with us

No matter how carefully or skillfully we drive, we cannot control the behavior of other road users. For those who travel frequently, the likelihood of road accidents naturally increases. This is precisely why motor insurance is critically important and increasingly essential in today’s world.

Another Reality: Insurance Companies May Not Act as Expected After an Accident

Although motor insurance is necessary, it must be acknowledged that when an accident occurs, many insurance companies may not act the same way they did when selling the policy.

Based on the experience of Wongsakorn Law Office, there are numerous cases in which insurance companies:

- Deny liability

- Offer compensation that is lower than the actual damages

- Or use technical policy conditions as an excuse to refuse claim payments

Many injured parties, despite being loyal customers who have paid premiums continuously, fail to receive fair treatment. As a result, many cases ultimately require legal consultation, as policyholders are unable to negotiate effectively with insurance companies on their own.

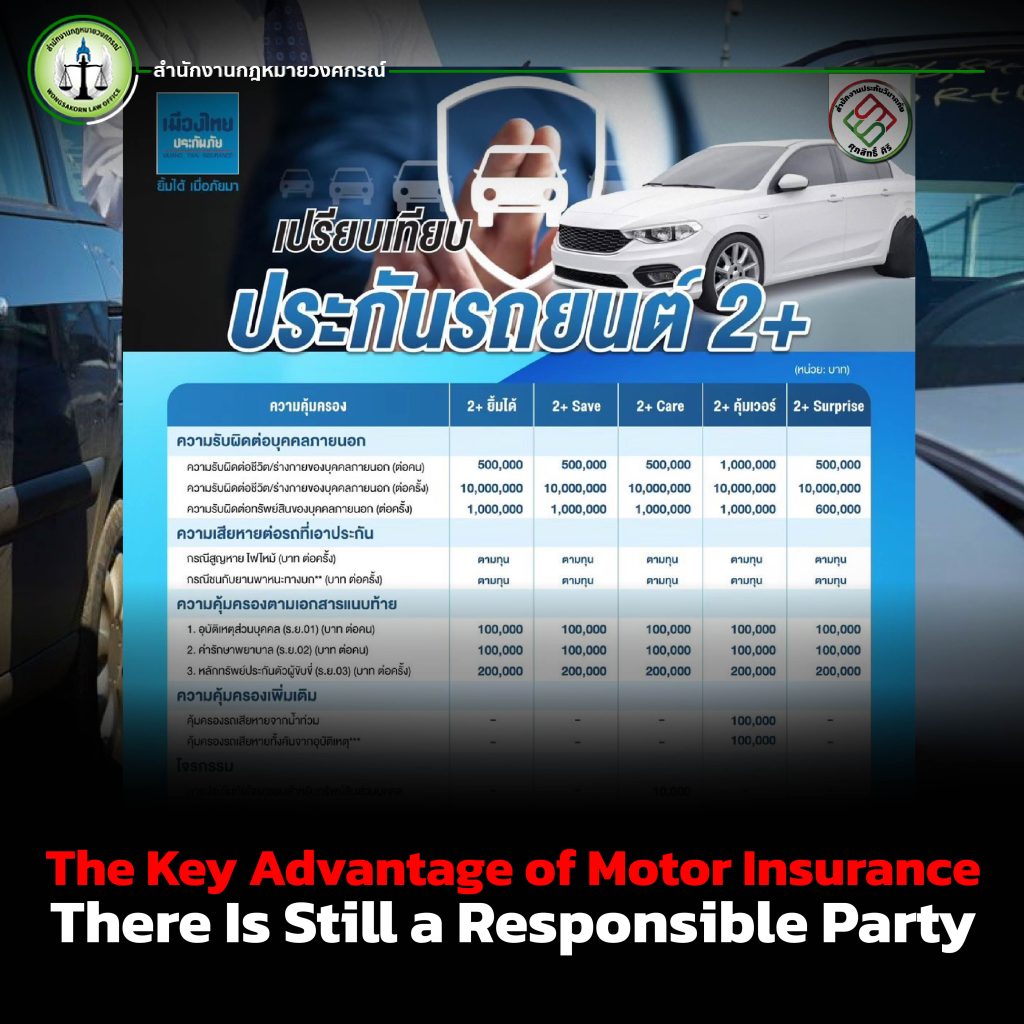

The Key Advantage of Motor Insurance: There Is Still a Responsible Party

Despite claim-related issues, motor insurance remains extremely important. Let us compare two scenarios clearly.

Case 1: You are hit by another vehicle, and the other party has insurance

You can directly claim compensation from the insurance company, which has the financial capacity and systems in place to handle damages.

Case 2: You are hit by another vehicle, and the other party has no insurance

Claiming compensation becomes immediately more difficult, especially if the other party claims they have “no money.” The situation may eventually lead to legal proceedings, which are time-consuming, costly, and often avoided by most people in Thailand.

As a result, many people choose to settle the matter:

- Out of sympathy for the other party

- Because the other party appears financially struggling

- Or with the mindset that “any compensation is better than none”

All of this clearly demonstrates that when the other party has motor insurance, everything becomes significantly easier.

Choosing Motor Insurance Wisely Requires Understanding Insurance Systems

Good motor insurance is not just about choosing the lowest premium or the highest coverage amount. It also requires:

- Understanding the rights of the insured

- Knowing the policy terms and conditions

- Having experts available for consultation when an accident occurs

In reality, insurance companies have legal teams supporting every claim. Policyholders should likewise have advisors who understand both the law and insurance systems, in order to avoid being placed at a disadvantage.

Motor Insurance That Offers More Than Coverage: Supasit Siri General Insurance Office Is the Answer

If you are looking for motor insurance that offers more than basic coverage and provides true peace of mind when accidents occur, Supasit Siri General Insurance Office is the answer.

Here, you will find a wide selection of motor insurance policies from leading insurance companies. More importantly, legal professionals are available to provide immediate consultation on legal and motor insurance matters when an accident happens. This ensures that you understand the insurance process, avoid being taken advantage of, and can properly assert your rights.

Good insurance should never leave you alone when an accident occurs.

Choose motor insurance from professionals who truly understand both law and insurance.

For motor insurance inquiries, please contact us or scan the QR Code to add Line and consult with us today.