Those who regularly follow legal content on the Wongsakorn Law Office website will notice that loss of use of a vehicle is one of the recurring legal issues that causes significant hardship to insured persons. Many cases reveal a troubling pattern in which insurance companies attempt to avoid liability or shift the burden onto policyholders, even though the damage results from accidents and repair processes beyond the insured’s control.

Loss of use of a vehicle is not a new legal concept. However, many consumers remain unaware of their legal rights, leading them to accept losses without receiving fair compensation. This article presents another real-life case that clearly illustrates why having a lawyer involved from the very beginning is critically important once damage occurs.

What Is “Loss of Use of a Vehicle”?

Loss of use of a vehicle refers to damages that a vehicle owner is legally entitled to claim when they are unable to use their vehicle under normal circumstances due to reasons not caused by their own fault for example, when the vehicle is damaged in an accident and must undergo lengthy repairs, preventing its use for work, business, or daily life.

Such damages may be claimed even if the injured party does not rent a replacement vehicle, provided it can be proven that the vehicle was normally in use and that the inability to use it caused actual damage. However, the method and effectiveness of claiming loss-of-use damages largely depend on the legal techniques and strategies employed by the lawyer handling the case, which can significantly affect the amount recoverable.

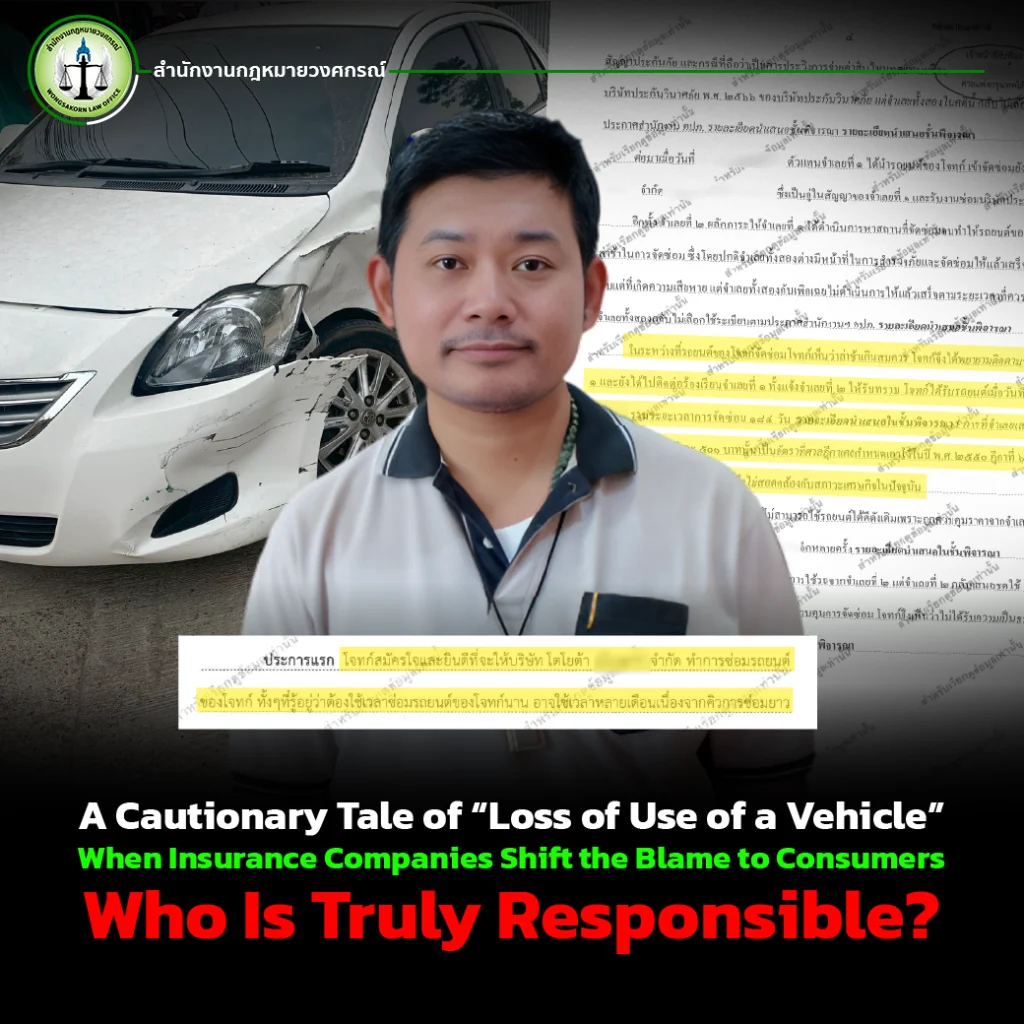

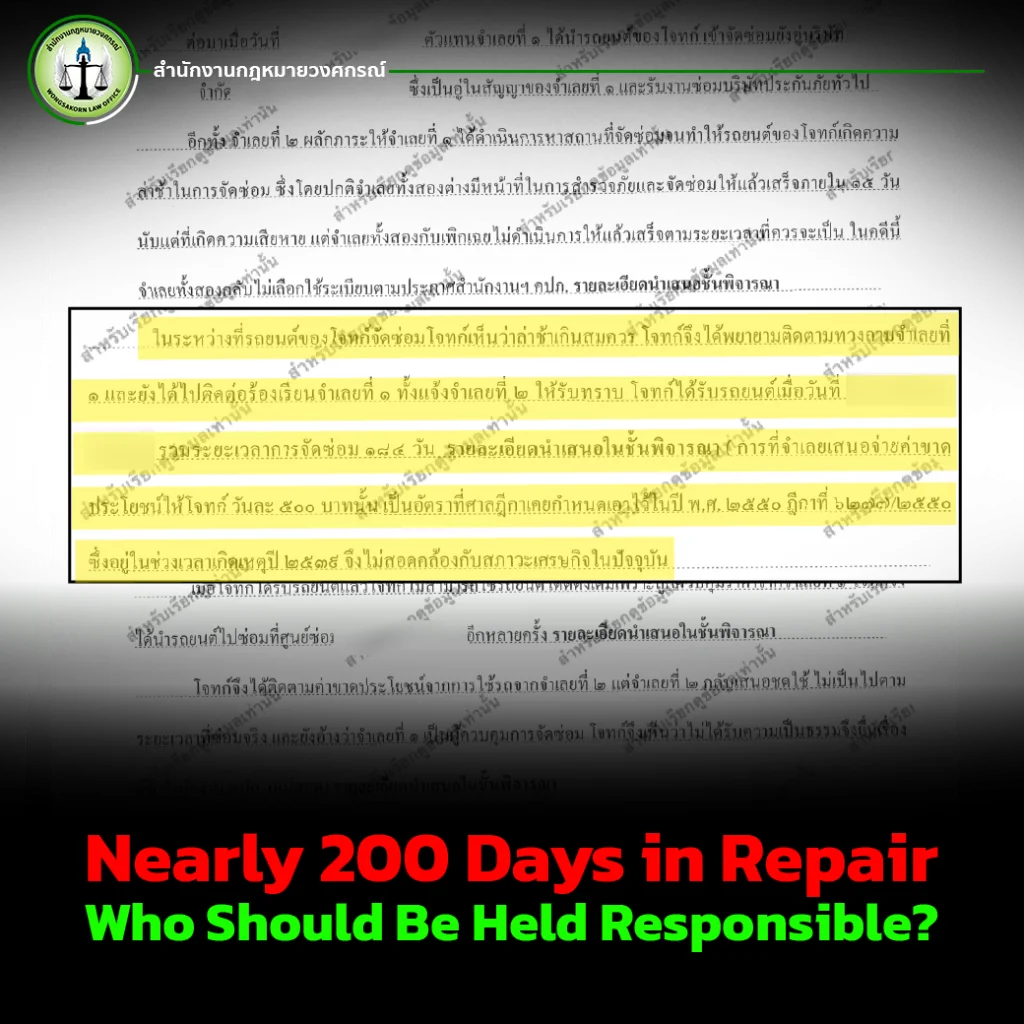

Nearly 200 Days in Repair Who Should Be Held Responsible?

In one illustrative case, the victim’s vehicle was severely damaged in an accident and required nearly 200 days of repair far exceeding a reasonable repair period. Due to this prolonged delay, the victim was unable to use the vehicle and therefore appointed a lawyer to pursue compensation, including loss-of-use damages, from the insurance company. However, what transpired in court raised serious concerns regarding the insurer’s conduct.

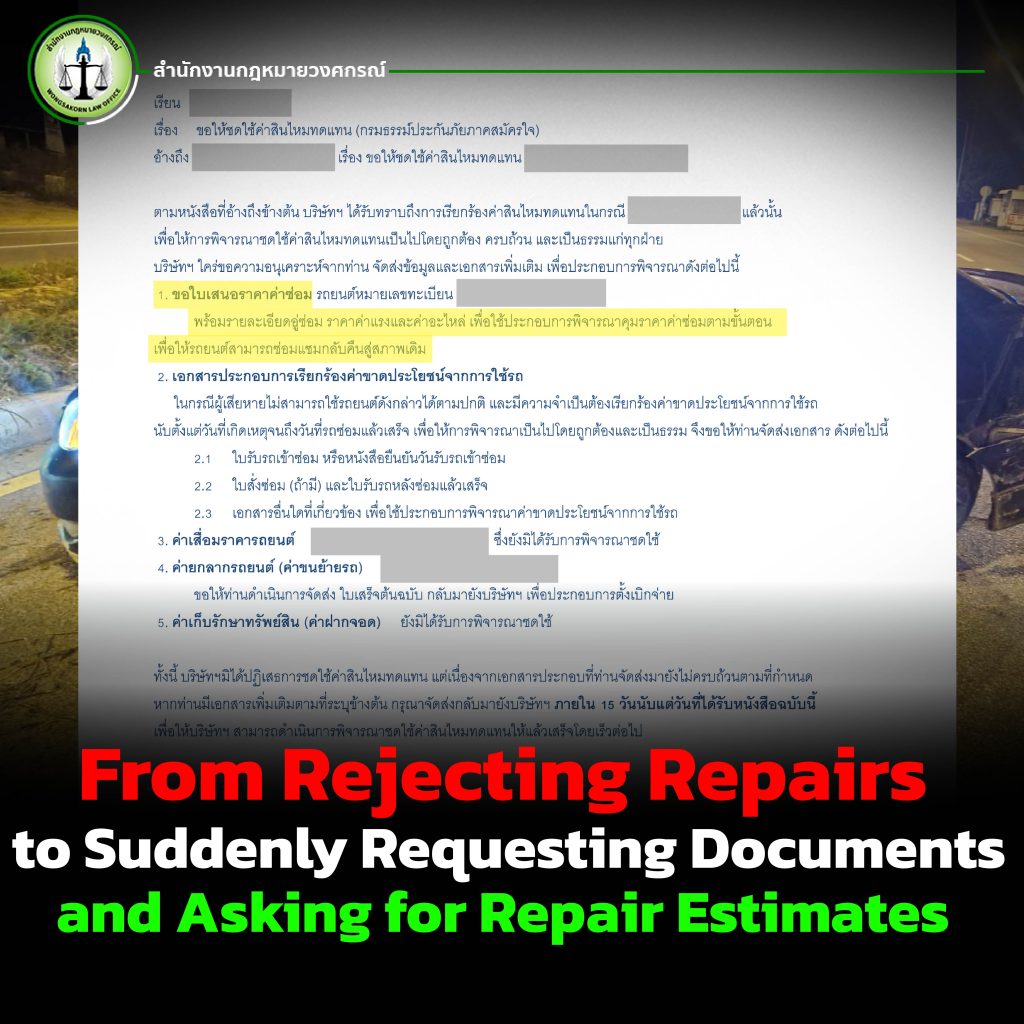

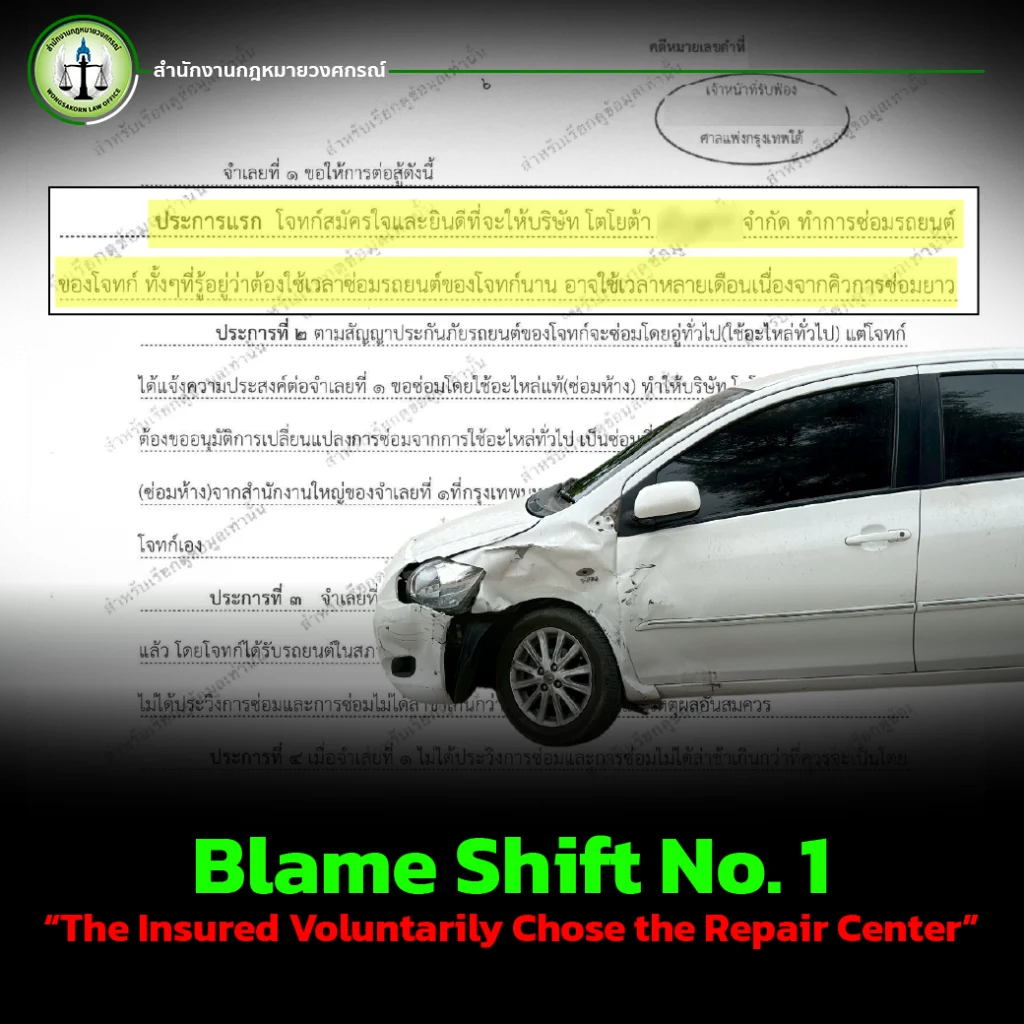

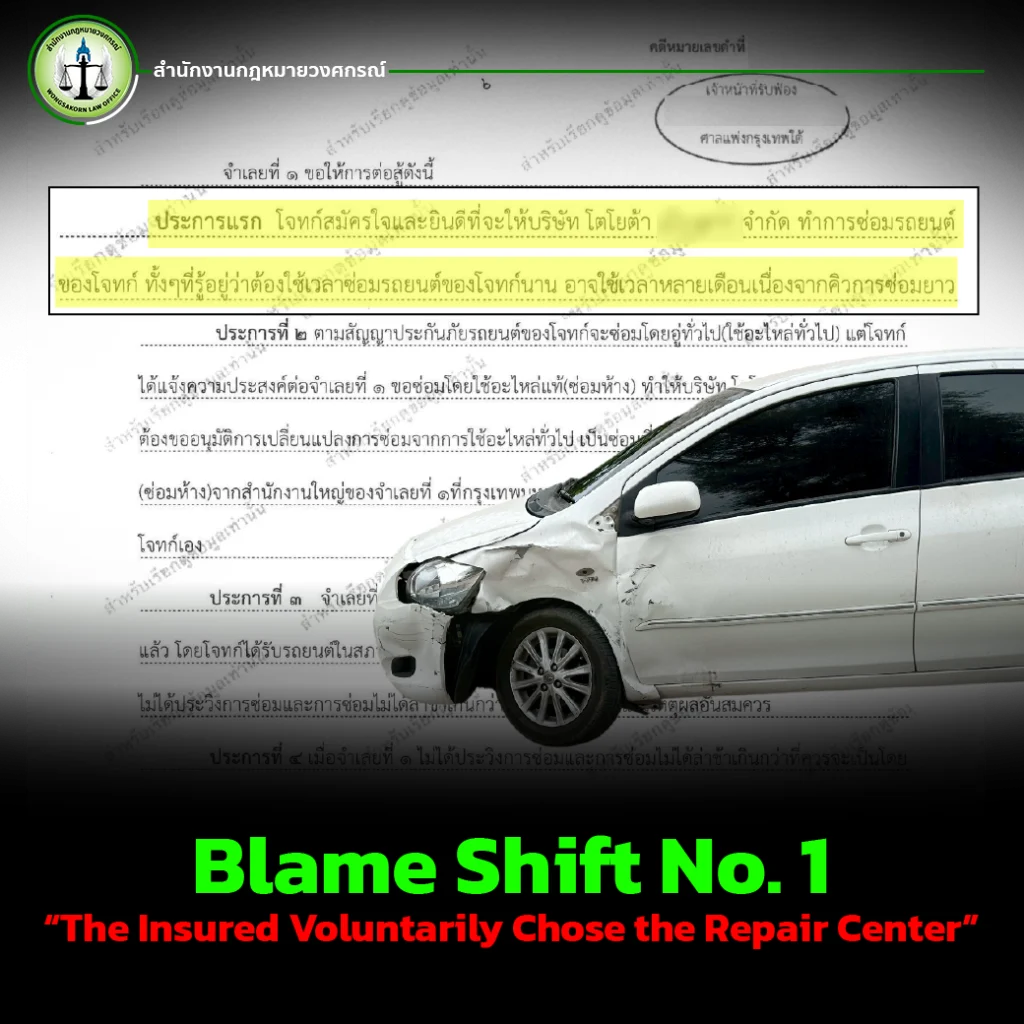

Blame Shift No. 1: “The Insured Voluntarily Chose the Repair Center”

The insurance company argued that:

“The plaintiff voluntarily chose to repair the vehicle at that service center, fully aware that the repair queue would take several months.”

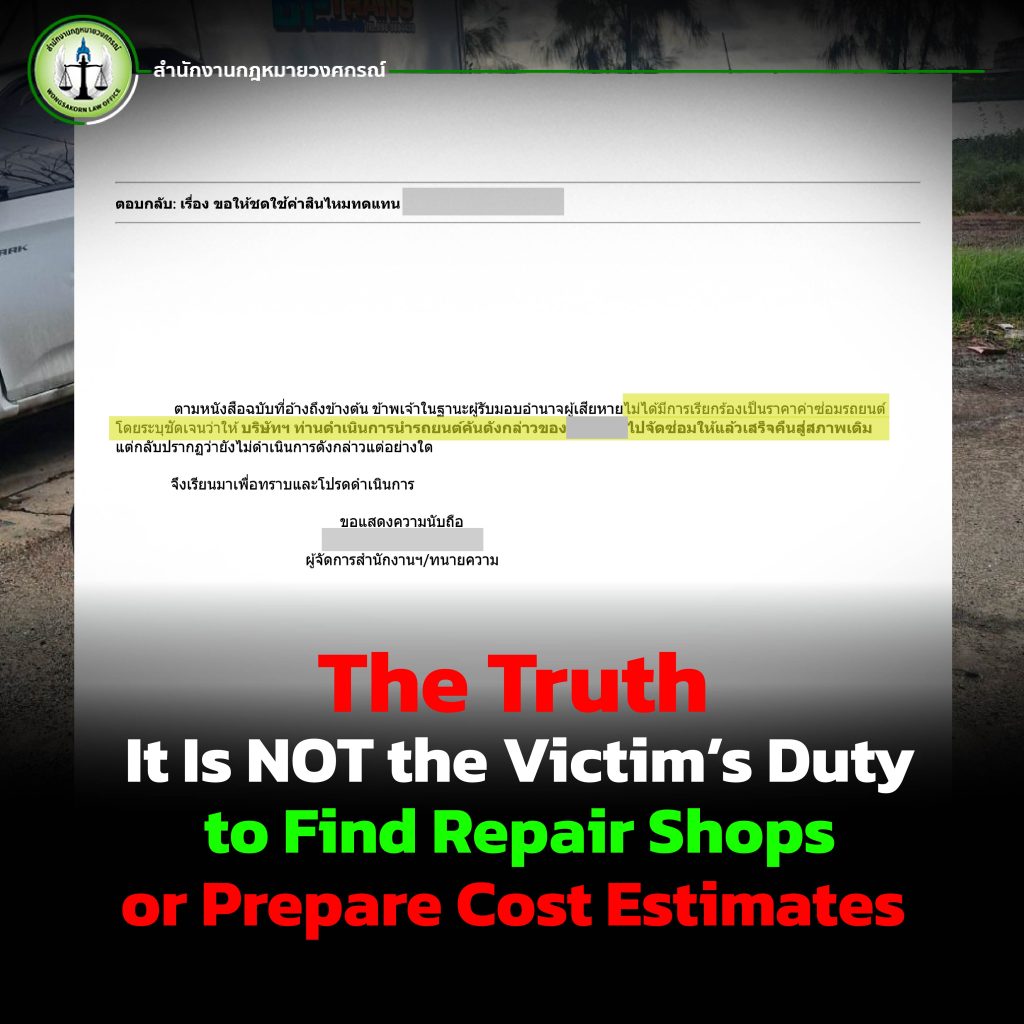

In other words, the insurer attempted to shift responsibility onto the insured, claiming that the insured must bear the consequences of the repair delay. In reality, insured persons often have little bargaining power and must rely on repair processes controlled by insurers, particularly regarding repair cost approvals.

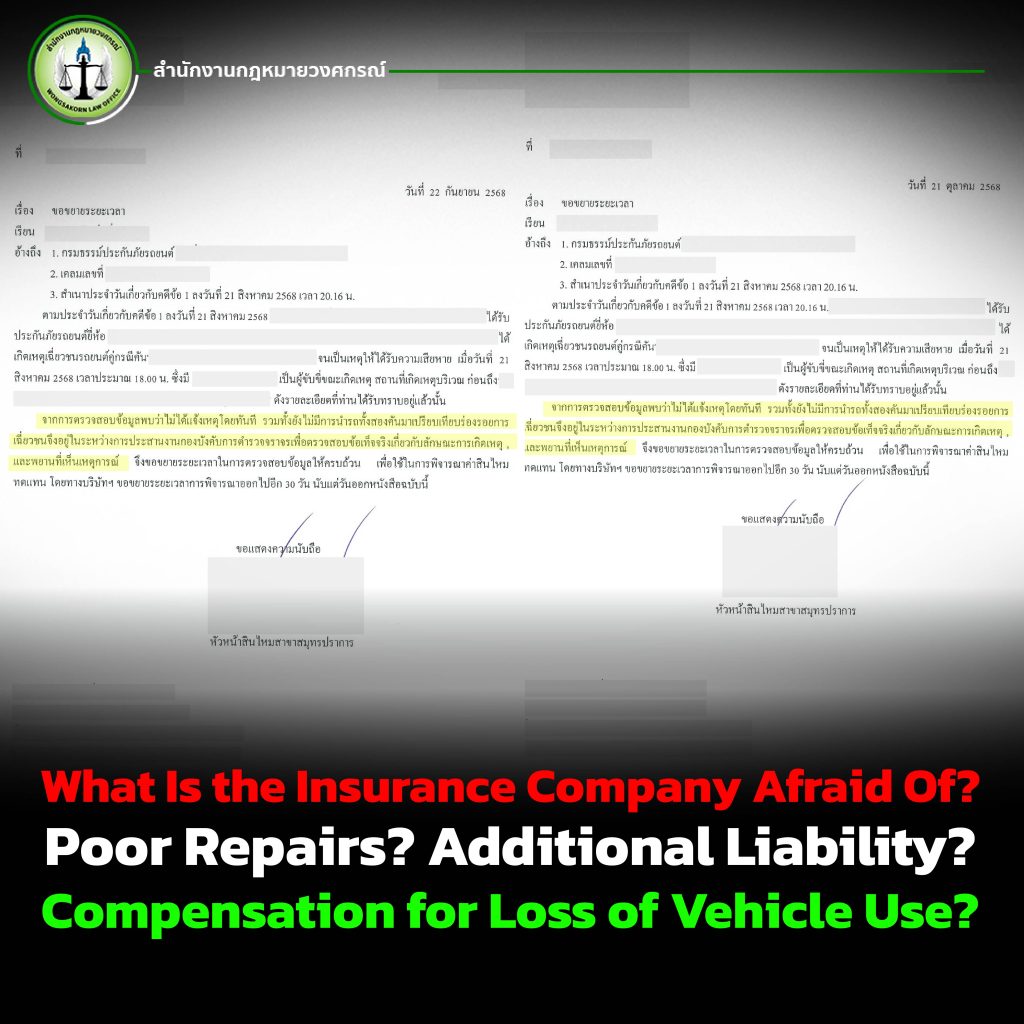

Blame Shift No. 2: Passing Responsibility to the Repair Center

After blaming the insured, the insurance company further shifted responsibility to the repair center, citing long repair queues. However, evidence showed that the insurer itself contributed to the delay through slow repair approval processes.

As a result, the insured was left in a situation where “no one takes responsibility,” despite being the insurer’s customer. This raises a crucial question: When should an insurance company, as the insurer, be held accountable to its policyholders?

Not Sure Where to Start After an Accident? Learn to Protect Yourself Through Wongsakorn Law Office’s YouTube Channel

After an accident, many people are unsure how to begin claiming loss-of-use damages, what to say to insurance companies, what documents are required, or whether the insurer’s explanations should be accepted. Numerous cases demonstrate that individuals who pursue claims on their own often face rejection, blame-shifting, or legal misinformation, ultimately giving up without fair compensation.

In truth, loss of use of a vehicle is a legally recognized right, and insurance companies cannot deny liability merely by citing long repair queues or claiming that the insured selected the repair center. The real issue is not the absence of rights, but the lack of knowledge on how to properly exercise them.

If you are unsure where to begin, we recommend following Wongsakorn Law Office’s YouTube channel, which offers real case studies, legal insights, and practical strategies regarding loss-of-use claims and insurance disputes in an easy-to-understand format empowering you to stay informed and avoid being taken advantage of.

Knowing your rights, knowing the techniques, and understanding insurance practices from the very first step can make all the difference.

Why Is It Crucial to Have a Lawyer from the Start?

This case clearly demonstrates the importance of involving a lawyer immediately after damage occurs. A lawyer can:

- Develop a compensation strategy from the outset

- Collect evidence regarding vehicle usage and repair duration

- Properly assess loss-of-use damages

- Prevent unfair denial of liability by insurance companies

In contrast, many victims first attempt to handle matters themselves and only consult a lawyer after repeated denials by which time they may have already lost critical legal advantages.

Consult a Lawyer Immediately Better Than Trying Alone and Receiving Nothing

This nearly 200-day repair case serves as a powerful reminder that victims should not bear the burden of delays and unfair treatment alone. Once damage occurs, insured persons’ rights deserve genuine protection.

If your vehicle has been in long-term repair or your loss-of-use claim has been denied, do not wait for the damage to escalate. You may consult a lawyer immediately to plan a fair, lawful, and strategic compensation claim from the very beginning. Consult a lawyer today Click “Contact Us”